Major Auto Insurers Raise Rates Based on

Economic Factors

Low- and Moderate-Income Drivers Charged Higher Premiums

June 2016

Douglas Heller

Michelle Styczynski

Major Auto Insurers Raise Rates Based on Economic Factors

Consumer Federation of America | Page 2

Introduction

All states except New Hampshire require drivers to purchase auto insurance, and the importance of

automobile ownership for most Americans adds a special responsibility to ensure fairness in the

auto insurance marketplace.

1

In most states, however, auto insurance premiums are driven in large

measure by economic factors that are unrelated to driving safety, a practice that most Americans

consider unfair. Among the most common of the individual economic and socio-economic

characteristics used by auto insurers are motorists' level of education, occupation, homeownership

status, prior purchase of insurance, and marital status. Because each of these factors are associated

with an individual's economic status and because insurers consistently use each factor to push

premiums up for drivers of lesser economic means, the combined effect of insurers' use of these

factors can result in considerably higher prices for low- and moderate-income Americans, leaving

many overburdened by unfairly high premiums and others unable to afford insurance at all.

For this study, Consumer Federation of America (CFA) tested premium quotes for men and women

in 15 cities across the country offered by the nation's five largest automobile insurers. Using a

methodology for distinguishing good drivers of lower and higher economic status, CFA was able to

determine how much more basic, liability-only auto insurance costs on average for drivers as a

result of these five non-driving related factors.

2

This study sheds new light on the cumulative

impact of auto insurance companies' pricing techniques and makes recommendations for

policymakers and regulators concerned about ensuring access to affordable auto insurance and

reducing the number of uninsured drivers.

In conjunction with this research, CFA also surveyed a representative sample of Americans

regarding the fairness of using various factors in the pricing of auto insurance. The results of this

survey offer new insights into the perspectives of consumers about insurance companies' use of

both driving related factors and non-driving related factors.

1

The requirement that drivers in every state but New Hampshire purchase auto insurance is compounded as an issue of social

concern because of the strong relationship between access to a car and employment rates, hours worked, and earnings. See, for

example: Charles L. Baum, “The Effects of Vehicle Ownership on Employment,” Journal of Urban Economics,” v. 66, n. 2,

151-163. Evelyn Blumenberg and Margy Waller, “The Long Journey to Work: A Federal Transportation Policy for Working

Families,” Center on Urban and Metropolitan Policy, Brookings Institute (July 20003).

2

There are other factors that drive up auto prices not analyzed here, the most important of which is credit-based scores. Another

rating factor that can impact rates and is related to economic status, the ZIP code in which the customer lives, was not measured

in this study, as all the drivers from each city were tested using the same address.

Major Auto Insurers Raise Rates Based on Economic Factors

Consumer Federation of America | Page 3

Summary of Findings

CFA has found that good drivers of lower economic status consistently pay significantly more for

auto insurance than higher economic status drivers. Four of five of the nation's largest auto

insurers regularly charge 40 percent to 92 percent more, or about $600 to $900 more per year, to

drivers based on factors related to their economic status even when they have perfect driving

records.

Among the findings:

A substantial majority of Americans believe it is unfair for insurance companies to use

economic characteristics – specifically, education level, occupation, not having insurance

because of not having a car, homeownership status, marital status, and credit score – in setting

auto insurance premiums.

Good drivers pay 59 percent more, or $681 annually, on average for auto insurance due to

personal characteristics associated with lower economic status.

GEICO and Progressive charge the largest average percentage increases (92 percent and 80

percent, respectively) to lower economic status drivers.

Allstate and Farmers charge the largest average annual dollar increases ($915 and $900,

respectively) to lower economic status drivers.

State Farm charges smaller increases to lower economic status drivers (13 percent, or $217

annually).

3

Drivers in Queens, Jersey City, Boston, Atlanta, Minneapolis, Houston, and Jacksonville face

some of the steepest increases, all of which average more than $700 more per year for good

drivers due to their economic status.

3

As is discussed, other research has shown that State Farm relies heavily on the use of credit scores, which can substantially raise

premiums on lower-income drivers.

Major Auto Insurers Raise Rates Based on Economic Factors

Consumer Federation of America | Page 4

Consumers believe auto insurance should be based on driving safety

factors and not economic characteristics

In June 2016, CFA commissioned ORC International to conduct a representative survey of 1,000

Americans to ascertain the public's view of the use of various rating factors in the setting of auto

insurance premiums. The survey found that 83 percent of the public found it very fair or somewhat

fair for auto insurers to use traffic accidents caused in setting premiums and 84 percent found it

very or somewhat fair to use moving violations such as speeding tickets. The near opposite was

true for the non-driving related factors that reflect drivers' economic status, as shown in Figure 2.

4

Respondents were asked the following question for each of the eight rating factors tested:

As you probably know, auto insurers use many factors to decide how much each driver is

charged for their insurance coverage. How fair do you think it is for insurers to use each of the

following factors in deciding on an auto insurance price for a driver? Would you say each is

very fair, somewhat fair, somewhat unfair or very unfair?

For the survey, the order in which the different factors were presented was randomized.

4

The survey of 1,006 Americans had a margin of error of +/- 3.09 percent at the 95 percent confidence level.

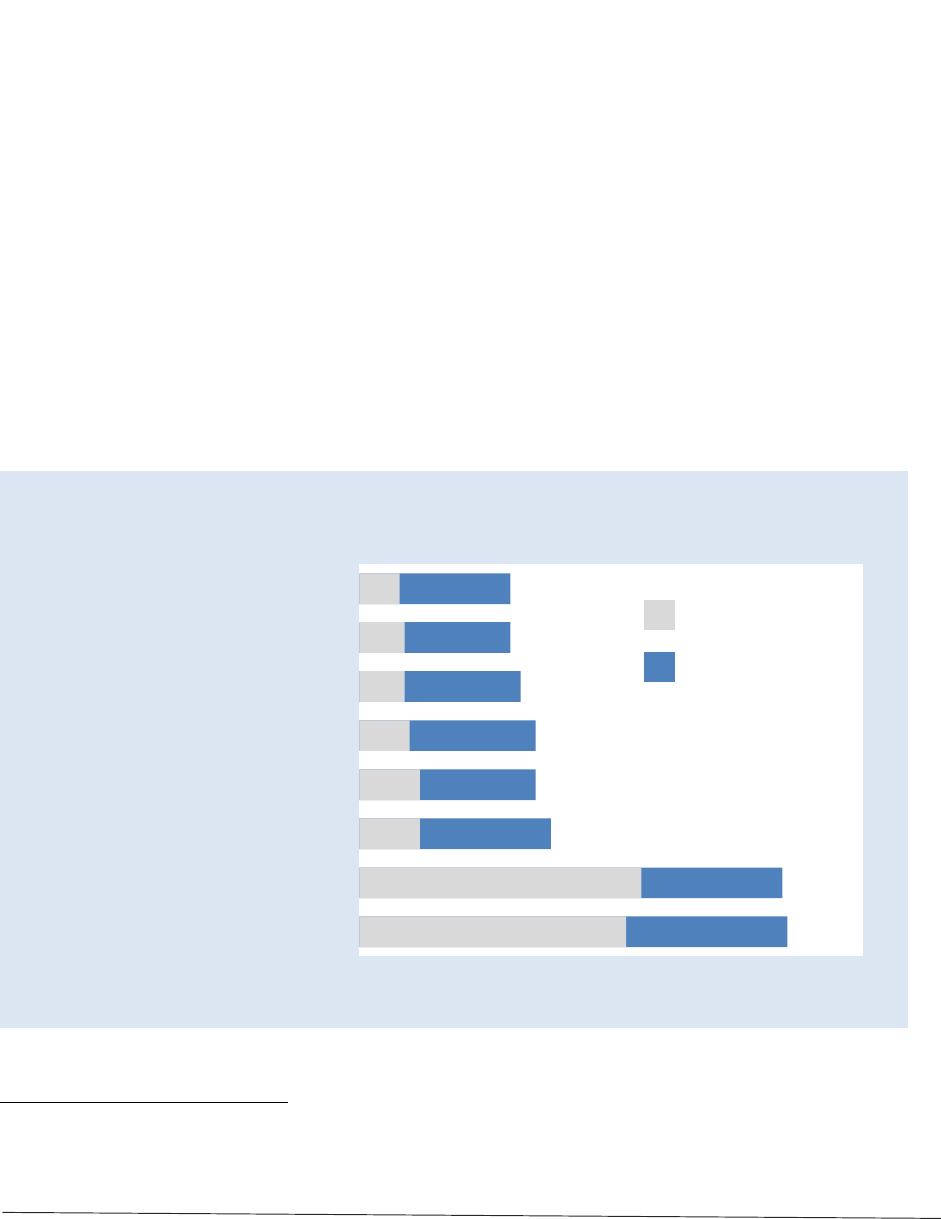

53%

56%

12%

12%

10%

9%

9%

8%

Moving violations

Traffic accidents caused

Credit scores

Homeownership

Occupation

Marital status

No previous insurance because no car

Level of education

Figure 1. Percentage of Americans who find each rating factor very fair or

somewhat fair

Source: ORC International Survey conducted June 9-12, 2016, all figures are rounded

21%

23%

25%

23%

26%

28%

32%

Somewhat fair

Very fair

22%

Major Auto Insurers Raise Rates Based on Economic Factors

Consumer Federation of America | Page 5

Only about one in 10 Americans think the use of these non-driving factors is "very fair." Conversely,

over six in ten Americans consider it somewhat or very unfair to use the non-driving factors

associated with economic status.

Data and Methodology

Prior Research

In previous reports, CFA collected premium quotes from individual companies' websites to assess

the impact of various rating factors on the price of auto insurance. Using this method, previous

research found, for example, that several major insurers charge significantly higher premiums to

drivers with only a high school diploma than to those drivers with higher levels of education, such

as a master’s degree.

5

Previous research also found that in many states, some major insurers

provide no discount, or only a minimal discount, to low-mileage drivers, despite the actuarial

evidence that annual mileage strongly correlates with risk of loss.

6

In 2014, CFA used a comprehensive dataset of auto insurance quotes for a typical moderate-income

good driver acquired from Quadrant Information Services to evaluate the availability and

accessibility of state-mandated auto insurance in lower-income communities in the 50 largest

metro areas. The report found that in approximately a third of lower-income ZIP codes none of the

largest insurers offered a basic policy for less than $500.

7

A later analysis of this data, published by

CFA in 2015, found that in communities where more than three quarters of the residents are

African American, auto insurance premiums average 70 percent higher than in those with

populations that are less than one quarter African American.

8

An analysis of similar Quadrant

Information Services data found that good drivers with low credit scores are charged as much as

127 percent more than drivers with high credit scores, controlling for all other factors including

driving record.

9

,

10

5

Brobeck, Stephen. “Use of Education, Occupation, and Other Non-Driving Factors Inflate Premiums for Low- and Moderate-

Income Drivers.” Washington, DC: Consumer Federation of America, September 24, 2012.

http://consumerfed.org/pdfs/PR.AutoInsuranceRateFactorRelease.9.24.12.pdf

6

Brobeck, Stephen, and Michelle Styczynski. “Auto Insurers Fail to Reward Low Mileage Drivers.” Washington, DC: Consumer

Federation of America May 21, 2015. http://consumerfed.org/news/902

7

Feltner, Tom, Stephen Brobeck, and J. Robert Hunter. “The High Price of Mandatory Auto Insurance for Lower Income

Households: Premium Price Data for 50 Urban Regions.” Washington, DC: Consumer Federation of America, September 2014.

http://consumerfed.org/pdfs/140929_highpriceofmandatoryautoinsurance_cfa.pdf.

8

Consumer Federation of America. "High Price of Mandatory Auto Insurance in Predominantly African American

Communities." November 2015.

9

Brobeck, Stephen, J. Robert Hunter, and Tom Feltner. “The Use of Credit Scores by Auto Insurers: Adverse Impacts on Low-

and Moderate-Income Drivers.” Consumer Federation of America, December 2013.

http://www.consumerfed.org/pdfs/useofcreditscoresbyautoinsurers_dec2013_cfa.pdf

10

Besides the studies discussed briefly above, CFA previously studied several rating factors individually and did other research

on the plight of low- and moderate-income affording state-required auto insurance. A list of all precious studies with thumbnail

Major Auto Insurers Raise Rates Based on Economic Factors

Consumer Federation of America | Page 6

Each of these studies laid the groundwork for the critical question we sought to answer in this

report: What is the cumulative impact of having socio-economic characteristics associated with low-

and moderate-income on the premiums paid by good drivers?

About the insurance premiums used in this report

For this report, CFA used the websites of the five largest auto insurers in the nation to determine

the premium that would be offered to four different drivers (two men and two women with

different socio-economic characteristics) in 15 cities across the country. The four drivers tested are

described in Figure 2.

In each case, the quotes are only for the minimum mandatory liability insurance that a driver is

required to carry in each state, except where a company did not offer state minimum limits

coverage through its website, as noted in the Appendix. CFA tested 300 drivers for this study and

received 259 online premium quotes; there were 20 tests where a company did not appear to

operate in a state and 21 instances where an insurer would not provide an online quote for lower

economic status drivers. All premiums were quoted for six-month policy terms and have been

annualized for this report.

Figure 2. About the driver profiles used in this study

All Drivers: 30 years old and licensed for 14 years; no accidents; no violations; drives a 2006 Toyota Camry

10,000 miles each year; all drivers have the same address for each city tested.

Female – High Economic Status: Bank executive

with a master's degree, is a homeowner, has had auto

insurance coverage with the same company for three

years, and is married.

Male – High Economic Status: Manufacturing

executive with a master's degree, is a homeowner, has

had auto insurance coverage with the same company for

three years, and is married.

Female – Low Economic Status: Bank teller with a

high school degree, is a renter, has not had auto

insurance for six months because she has not had a

car, and is single.

Male – Low Economic Status: Factory worker with a

high school degree, is a renter, has not had auto

insurance for six months because he has not had a car,

and is single.

descriptions can be found at http://consumerfed.org/cfa-studies-on-the-plight-of-low-and-moderate-income-good-drivers-in-

affording-state-required-auto-insurance

Major Auto Insurers Raise Rates Based on Economic Factors

Consumer Federation of America | Page 7

When shopping for auto insurance most consumers find that insurance companies request a range

of personal information that is unrelated to their driving history or car they wish to insure. It is

unlikely, however, that many of these shoppers are aware of the extent to which their answers to

these questions impact the price they will pay for auto insurance. There are five common questions

asked by auto insurers that are not driving-related and tend to be good indicators of a customer's

economic status:

1. Are you married? Unmarried people have lower incomes than married people.

2. What is your occupation? Blue collar and hourly workers have lower incomes than white collar

and salaried workers.

3. What is your highest level of education? Lower levels of education are associated with lower

income.

4. Do you currently have auto insurance? Whether because a driver did not have a car for a period

of time or because their coverage lapsed, drivers without current insurance tend to have lower

incomes. (In the data collected as part of this study, the lower economic status drivers did not

have a car for the past 6 months).

5. Do you own or rent your home? The median income of renters is less than half that of

homeowners.

As is discussed below, this report shows that, with almost no variation, the price charged to

consumers is inversely related to the economic indication associated with their answers to these

five questions. In this report, CFA has calculated the cumulative impact of these non-driving related

factors for basic liability-only policies that drivers in all states except New Hampshire are required

to purchase.

Another typical question – what is your social security number? – provides insurers with the

information they need to incorporate drivers' credit scores into premiums, with the same inverse

relationship in which premiums go up as credit scores (another indicator of economic status) go

down. Though this factor was not tested in this study, a 2015 Consumer Reports study found that

premiums rose significantly for drivers with low credit scores.

11

Inclusion of credit scores would

further increase the disparities found in this report in every city except Boston and Los Angeles

where auto insurance credit scoring is prohibited.

11

http://www.consumerreports.org/cro/car-insurance/credit-scores-affect-auto-insurance-rates/index.htm CFA also found similar

results in a 2013 study: Brobeck, Stephen, J. Robert Hunter, and Tom Feltner. “The Use of Credit Scores by Auto Insurers:

Adverse Impacts on Low- and Moderate-Income Drivers.” Washington, DC: Consumer Federation of America, December 2013.

http://www.consumerfed.org/pdfs/useofcreditscoresbyautoinsurers_dec2013_cfa.pdf

Major Auto Insurers Raise Rates Based on Economic Factors

Consumer Federation of America | Page 8

Analysis and Findings

On average, a high economic status driver is charged $1,144 per year for a minimum limits policy

offered by the five companies tested in 15 cities. A low economic status driver with the same

driving record and living at the same address is charged a premium of $1,825 on average for the

same coverage. That difference, $681 per year, amounts to a 59 percent penalty that insurers

impose on good drivers based solely on their answers to the five economic status questions

described above.

Where companies provided quotes for both the higher and lower economic status driver, the driver

with the lower economic status characteristics faced a premium increase 92 percent of the time.

Those drivers were charged at least 25 percent more two-thirds of the time, and a fifth of the lower

economic status drivers paid at least double that of his or her higher status counterpart, despite

having the same driving record, driving the same car, being the same age, having driven for the

same number of years and living at the same address. There were only three instances (about 1

percent) in which the lower economic status driver paid less than the higher economic status

driver.

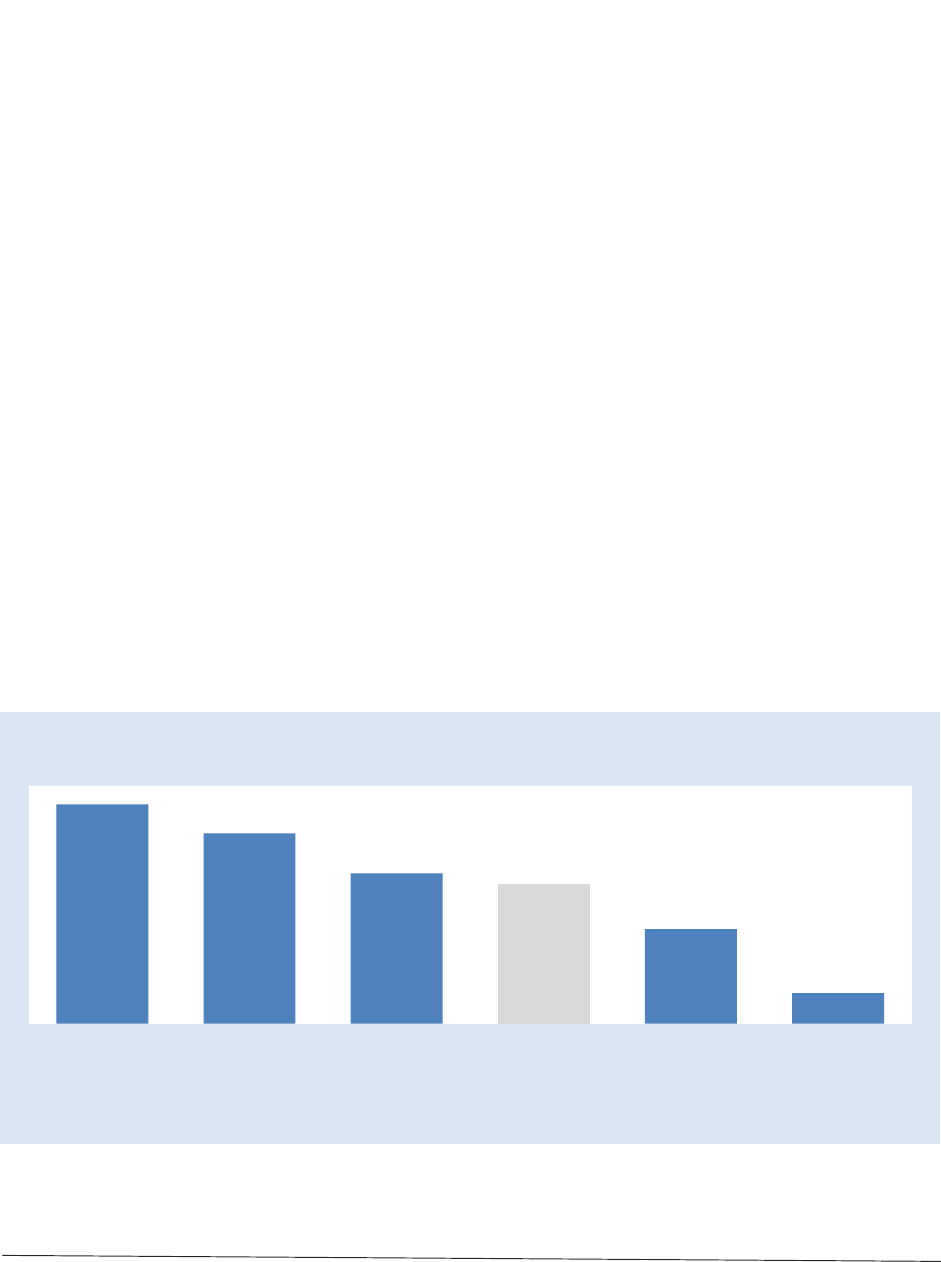

On a nationwide basis, GEICO imposed the largest average premium hikes by percentage on good

drivers with lower socio-economic indicators (92 percent increase), and State Farm increased rates

the least based on the factors tested (13 percent), as shown in Figure 3. We note, however, that

according to the 2013 CFA report on credit scoring in auto insurance cited above, State Farm used

credit scoring to raise rates on drivers with the lowest credit scores by 127 percent on average over

those with the best credit scores. That impact cannot be captured through the website testing

methodology used for this report since it would require the use of a Social Security number.

92%

80%

63%

59%

40%

13%

GEICO Progressive Farmers Average of all

quotes

Allstate State Farm

Source: CFA premium testing, see Appendix

Note 1: Excludes city data where company does not provide quote to lower economic status driver

Figure 3. 15 city average increase for lower economic status drivers by company

Major Auto Insurers Raise Rates Based on Economic Factors

Consumer Federation of America | Page 9

As noted above, the lower economic status driver in the cities tested pays $681 more per year on

average for a basic auto insurance policy than drivers with the same good driving record but with a

higher economic status. While GEICO and Progressive show the largest economic status penalties

as a percentage of premium, the dollar impact, shown in Figure 4, is the largest for customers of

Farmers and Allstate, which charged substantially higher premiums overall than the other three

companies tested.

The wide variation in premiums among companies noted above, while not the central focus of this

report, is notable. As a review of the Appendix reveals, the price offered to the same driver buying

the same coverage in the same city can vary dramatically from company to company. For example,

in Minneapolis, State Farm charges a low economic status male driver $994 per year for a minimum

limits policy, while Farmers charges the same driver $3,626 per year. Similarly, in Baltimore a low

economic status female driver is quoted a premium of $1,232 by GEICO, but the exact same driver

faces a $2,544 premium from Progressive.

$915

$900

$830

$681

$614

$217

Allstate Farmers Progressive Average of all

quotes

GEICO State Farm

Figure 4. 15 city average annual increase in dollars for lower economic status drivers,

by company

Source: CFA premium testing, see Appendix

Note 1: Excludes city data where the company did not provide a quote to the lower economic status driver

Note 2: Allstate's Jersey City and Boston quotes are for coverages higher than the basic limits policy mandated by

state laws, because the company did not quote minimum limits-only policies online in those cities.

Major Auto Insurers Raise Rates Based on Economic Factors

Consumer Federation of America | Page 10

Drivers in all cities but Los Angeles pay at least 33 percent more on average due to

non-driving related, economic status factors; some pay much more

Drivers face steep rate hikes in every city tested due to economic status factors, with the exception

of Los Angeles as is discussed below. The largest increase on a percentage basis was the 309

percent premium hike for a female driver in Minneapolis handed out by GEICO. While the

companies varied in the degree to which they punished good drivers based on economic status

indicators, there were at least two instances for each company in which the economic status

penalty exceeded $1,000 per year. Figure 5 shows the two largest rate hikes in the cities tested for

customers of each company.

Figure 5. Largest increases by company

Company

City

High Status

Premium

Low Status

Premium

Increase

Percent

$

Allstate*

Jersey City, NJ (Female)

Jersey City, NJ (Male)

$3,138

3,150

$8,906

8,358

184%

165

$5,768

5,208

Farmers

Houston, TX (M)

Houston, TX (F)

1,380

1,408

3,390

3,218

146

129

2,010

1,819

GEICO

Minneapolis, MN (F)

Minneapolis, MN (M)

528

528

2,158

1,840

309

248

1,630

1,312

Progressive

Queens, NY (F)

Atlanta, GA (F)

2,174

764

6,668

2,000

207

162

4,494

1,236

State Farm

Queens, NY (M)

Queens, NY (F)

2,438

$2,388

4,144

$3,974

70

66%

1,706

$1,586

Source: CFA premium testing, see Appendix

*Note: Allstate does not offer a New Jersey minimum limits policy through its website; NJ Allstate quotes are for the lowest liability

coverage (50/100) available online

As can be seen in Figure 6, the lower economic status driver pays substantially more on average (at

least $200) for basic auto insurance in every city except Los Angeles. Drivers in Atlanta, Baltimore,

Boston, Houston, Jacksonville, Kansas City, and Minneapolis pay more than $500 per year extra for

having the characteristics of lower economic status. In the highest cost cities of Jersey City and

Queens

12

, lower economic status drivers pay an average $1,815 and $1,856 more, respectively,

despite their good driving record.

12

The tests for Queens, NY, were for a driver living in the Far Rockaway neighborhood.

Major Auto Insurers Raise Rates Based on Economic Factors

Consumer Federation of America | Page 11

Figure 6. Average premium for good drivers with different economic status characteristics, by city

High Status

Low Status

Difference ($)

Change (%)

Queens, New York

$1,912

$3,769

$1,856

97%

Atlanta, Georgia

938

1,800

862

92

Kansas City, Missouri

662

1,241

579

87

Jacksonville, Florida

908

1,659

751

83

Jersey City, New Jersey

2,333

4,148

1,815

78

Boston, Massachusetts

1,062

1,801

739

70

Houston, Texas

1,063

1,800

737

69

Minneapolis, Minnesota

1,539

2,394

856

56

Seattle, Washington

854

1,309

456

53

Phoenix, Arizona

853

1,264

411

48

Baltimore, Maryland

1,644

2,272

628

38

Oklahoma City, Oklahoma

859

1,155

296

34

Pittsburgh, Pennsylvania

724

963

240

33

Chicago, Illinois

697

925

228

33

Los Angeles, California

$859

$939

$80

9%

Average of all quotes

$1,144

$1,825

$681

59%

Source: CFA premium testing, see Appendix

Note 1: Excludes city data where company does not provide quote to lower economic status driver

The only instances where premiums came down for drivers were from Allstate, which lowered

rates by 19 percent for the lower economic status female driver in Chicago and by 4 percent for

both male and female drivers in Oklahoma City. These represent about 1 percent of all quotes

offered by the companies tested in the fifteen cities.

The average percentage increase paid by lower economic status drivers in each city is shown in

Figure 7.

Major Auto Insurers Raise Rates Based on Economic Factors

Consumer Federation of America | Page 12

As can be seen in the Figure 7, Los Angeles is the only city with very little difference between the

lower economic status driver and the upper economic status driver. That is because all of the non-

driving factors tested in this report are prohibited from use in auto insurance pricing in California

with the exception of marital status, which accounts for the 9 percent, or $80 per year, average

premium difference seen in Los Angeles.

No online quotes for some lower economic status drivers

Of the 280 drivers for whom CFA sought price quotes (putting aside the situations where a

company did not do business in a selected state), there were 21 instances in which a company

would not provide a quote to the driver with lower economic status characteristics. In those cases,

although the company would, for example, provide a quote to the married male executive with a

masters degree who owned his home and had current auto insurance with another company, the

company refused to provide an online quote to the unmarried male factory worker with a high

school degree who rents his home and does not have current auto insurance. There were no

instances in which the high economic status driver was not quoted a premium when the lower

status driver was offered a quote.

9%

33%

33%

34%

38%

48%

53%

56%

69%

70%

78%

83%

87%

92%

97%

Los Angeles, CA

Chicago, IL

Pittsburgh, PA

Oklahoma City, OK

Baltimore, MD

Phoenix, AZ

Seattle, WA

Minneapolis, MN

Houston, TX

Boston, MA

Jersey City, NJ

Jacksonville, FL

Kansas City, MO

Atlanta, GA

Queens, NY

Figure 7. Average rate hike for lower economic status drivers, by city

Source: CFA premium testing, see Appendix

Major Auto Insurers Raise Rates Based on Economic Factors

Consumer Federation of America | Page 13

Figure 8 shows the instances in which high status drivers were offered a policy online but low

status drivers with good driving records were not offered a quote through a company website.

Figure 8. Tests resulting in no online quote offered to lower economic status driver

Allstate

State Farm

Farmers

Baltimore

M

Atlanta

M,F

Baltimore

M

Boston

M,F

Chicago

M

Pittsburgh

M,F

Jacksonville

M,F

Kansas City

M,F

Kansas City

M,F

Phoenix

M,F

Queens

M,F

Seattle

M,F

Note: M = Male, F = Female

Because companies did not offer online quotes to the lower economic status driver in these 21

instances, we had to exclude the premium offered to the higher economic status counterpart from

all calculations. CFA did not test whether these companies would offer coverage to the lower

economic status driver if he or she contacted the insurance company by phone or in person.

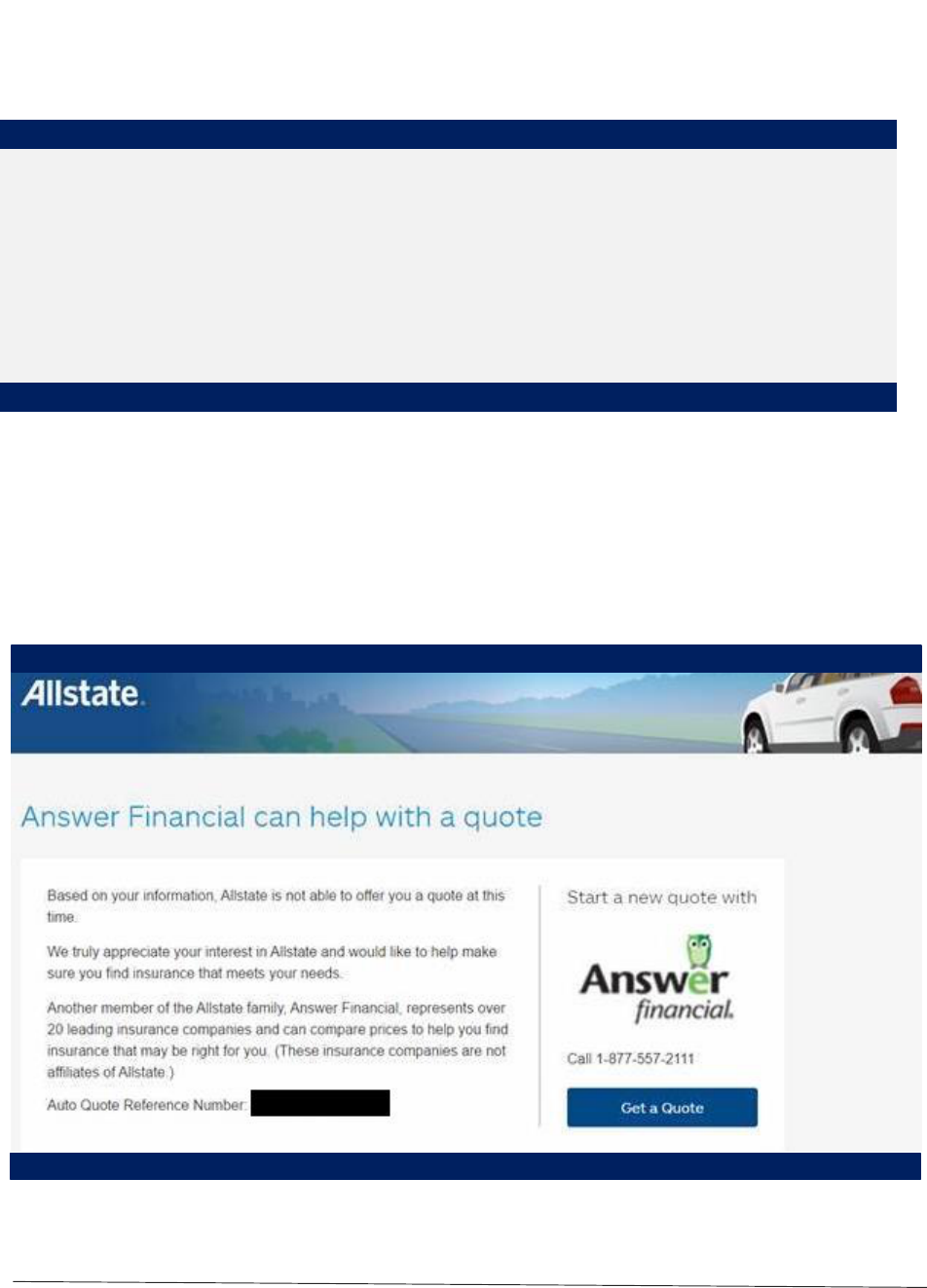

Figure 9 provides one example where a low economic status driver was refused an online quote.

Figure 9. In some cities low economic status drivers are refused an online premium quote

Major Auto Insurers Raise Rates Based on Economic Factors

Consumer Federation of America | Page 14

In addition to refusing to quote lower economic status drivers, there were several instances where

customers with lower economic status characteristics were not offered policies from the standard

insurance company but, instead, from an affiliated company. This study did not determine if these

companies would have charged a lower rate had the customer been offered a policy from the

standard company or if, in some cities, the companies only write policies for lower economic status

drivers through their non-standard affiliates.

Conclusion

The basic liability insurance that drivers in all states but New Hampshire must purchase presents a

difficult financial challenge for many low- and moderate-income Americans. That difficulty is

exacerbated by an insurance pricing system that punishes good drivers through the use of non-

driving related factors that are strong indicators of customers' economic status. As a result:

good drivers with lower levels of education pay more;

good drivers with blue collar, low-skilled and semi-skilled jobs pay more;

good drivers who rent their homes rather than own pay more;

good drivers who had a break in coverage because they didn't have a car pay more; and

good drivers who are single rather than married pay more.

When taken together, the cumulative impact of these non-driving rating factors pushes rates up by

59 percent, or $681, each year for drivers with perfect driving records but non-driving

characteristics that suggest a lower economic status in society.

These pricing practices, common among most major carriers, as well as the use of credit scoring,

are rejected as unfair by a substantial majority of Americans. Most Americans believe that it is fair

to set rates based upon driving-related factors such as accidents caused and traffic violations but

not based on the non-driving related factors tested in this study.

Major Auto Insurers Raise Rates Based on Economic Factors

Consumer Federation of America | Page 15

Recommendations

With an estimated 15 percent of Americans driving uninsured and facing stiff penalties if caught

(and forcing up the price of uninsured motorist coverage), and millions more struggling with the

high cost of auto insurance, it is incumbent upon policymakers and regulators to implement

consumer protections that prohibit the use of non-driving rating factors.

1. Regulators need to more seriously address the impact of auto insurance pricing methods

on lower-income drivers. This requires that more attention be paid to the use of non-driving

rating factors that, cumulatively, result in dramatically higher prices for lower-income good

drivers

State insurance regulators should require all companies to provide a series of

premium examples that show the impact of non-driving rating factors. Departments of

Insurance should require each company to publicly disclose the premium that would be

charged to good drivers under scenarios that reflect differences only in non-driving,

economic characteristics, such as those discussed in this report.

The Federal Insurance Office (FIO) should review the affordability and accessibility of

state-mandated minimum liability coverage in low- and moderate-income communities

and communities of color. This review should be based on premium data collected directly

from insurers for a series of driver profiles that are reflective of typical lower-income

drivers and include premiums from both the standard and non-standard markets. FIO

issued a request for information in April of 2014 and a second request for information in

June 2015. We urge the completion of an affordability review in 2016.

13

The National Association of Insurance Commissioners should develop a model data

call that will assist state regulators and legislators to better understand the premiums

charged to low- and moderate-income drivers. Such a model would require insurers to

provide premiums charged to drivers with certain economic characteristics typical of these

drivers, such as those described in this report.

13

For more information on data collection recommendations please see comments filed in response to the Federal Insurance

Office Request for Information Monitoring Availability and Affordability of Auto Insurance (TREAS-DO-2015-0005) filed by

49 consumer, community and civil rights organizations and available for review at

http://www.consumerfed.org/pdfs/150831_TREAS-DO-2015-0005_FIO_consumercomments.pdf.

Major Auto Insurers Raise Rates Based on Economic Factors

Consumer Federation of America | Page 16

2. State lawmakers should enact consumer protection reforms that prohibit the use of

economic status factors and make auto insurance more affordable for lower-income

drivers.

States should enact legislation that emphasizes drivers' accident and ticket records

and prohibits the use of non-driving related characteristics such as those discussed in this

report.

States should require insurers to offer drivers with clean driving records a quote

online irrespective of their non-driving related characteristics and offer the lowest

premium for which they qualify from among the company’s affiliates doing business in

the state. All drivers are required to purchase insurance, so insurers should be required to

provide good drivers the same access to the marketplace and treated in the same manner

regardless of their economic status. Additionally, customers with a safe driving record

should not be foisted to higher priced company affiliates based solely on non-driving

related factors related to their economic status. Any driver with a good driving record

should be offered the opportunity to purchase coverage from the affiliate that yields the

lowest premium for that coverage. Currently, only California has this “best price”

requirement for good drivers.

States should consider establishing programs that provide minimal liability coverage

to safe lower-income drivers at an affordable price sufficient to fund claims covered by

the program without subsidy. Knowing that even a reformed system will still be out of reach

to some low-income drivers, states should look at multiple ways to address the large

number of uninsured drivers; California offers such a program that sells policies to lower-

income drivers for between $241 and $428 per year, without requiring subsidy from other

drivers or taxpayers. This is possible since only lower-income drivers with good driving

records qualify for the program.

Major Auto Insurers Raise Rates Based on Economic Factors

Consumer Federation of America | Page 17

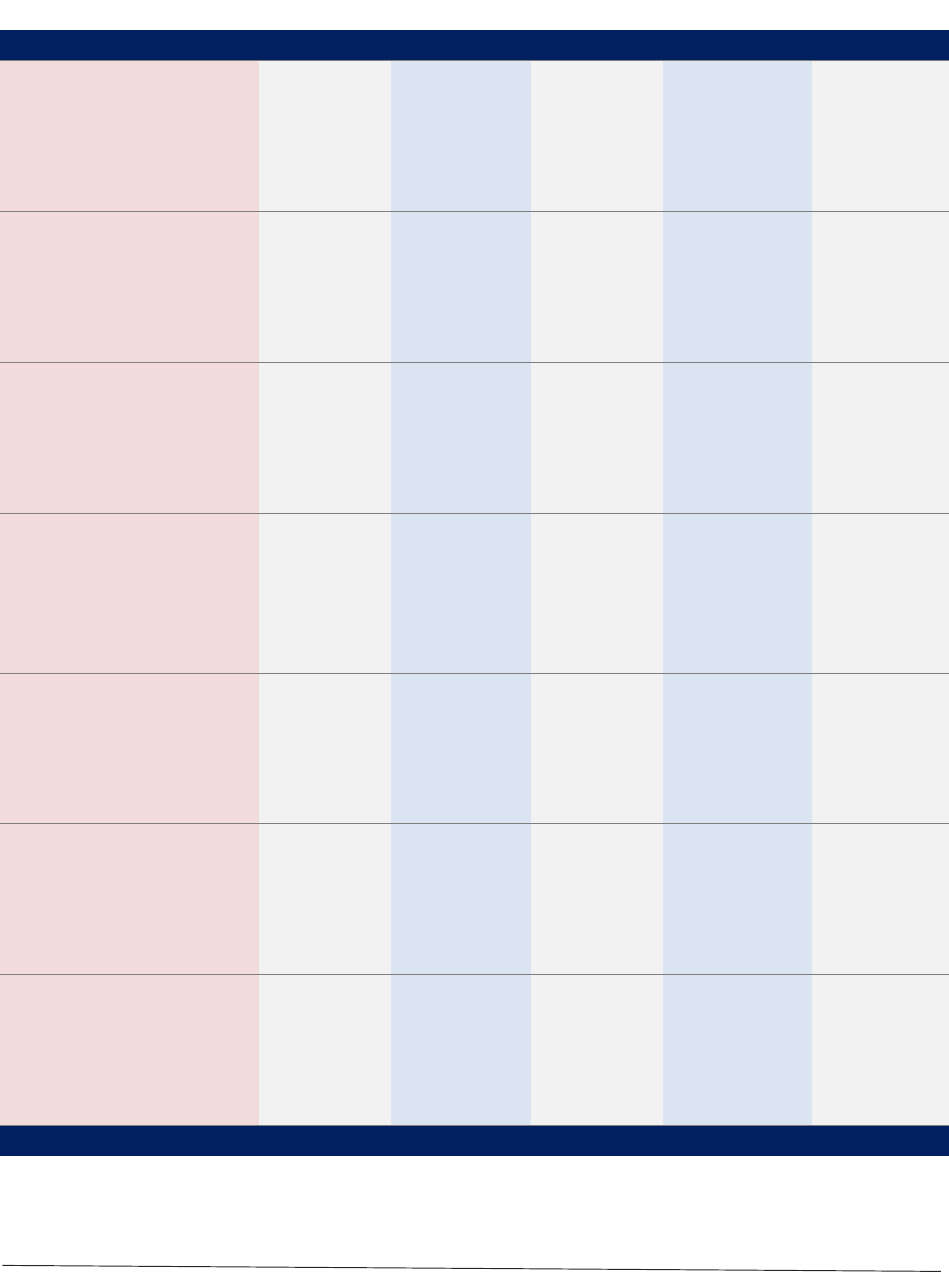

Appendix

Annual premium by city, driver profile and insurer

Atlanta, GA

GEICO

Progressive

Allstate

State Farm

Farmers

High Status Female

$790

$764

$1,298

$1,446

N/A

Low Status Female

$1,920

$2,000

$1,442

N/Q

N/A

High Status Male

$790

$752

$1,234

$1,514

N/A

Low Status Male

$2,082

$1,896

$1,460

N/Q

N/A

Baltimore, MD

High Status Female

$828

$1,534

$1,614

$1,434

$2,300

Low Status Female

$1,232

$2,544

$1,770

$1,484

$3,404

High Status Male

$1,004

$1,582

$1,556

$2,858

$2,726

Low Status Male

$2,400

$2,380

N/Q

$2,960

N/Q

Boston, MA

High Status Female

$722

$1,402

$2,536

N/A

N/A

Low Status Female

$1,348

$2,254

N/Q

N/A

N/A

High Status Male

$722

$1,402

$2,536

N/A

N/A

Low Status Male

$1,348

$2,254

N/Q

N/A

N/A

Chicago, IL

High Status Female

$474

$328

$582

$434

$744

Low Status Female

$560

$504

$472

$448

$1,030

High Status Male

$690

$596

$750

$876

$1,674

Low Status Male

$778

$1,084

$1,398

N/Q

$2,054

Houston, TX

High Status Female

$944

$686

$1,124

$1,286

$1,408

Low Status Female

$1,652

$1,374

$1,396

$1,326

$3,218

High Status Male

$732

$688

$1,100

$1,286

$1,380

Low Status Male

$1,552

$1,310

$1,456

$1,326

$3,390

Jacksonville, FL

High Status Female

$868

$882

$2,860

$956

N/A

Low Status Female

$2,004

$2,224

N/Q

$1,470

N/A

High Status Male

$868

$918

$2,860

$956

N/A

Low Status Male

$1,032

$1,752

N/Q

$1,470

N/A

Jersey City, NJ

High Status Female

$618

$1,546

$3,138

$2,696

$3,830

Low Status Female

$1,562

$2,440

$8,906

$2,792

$5,968

High Status Male

$618

$1,206

$3,150

$2,696

$3,830

Low Status Male

$1,388

$1,916

$8,358

$2,792

$5,354

Major Auto Insurers Raise Rates Based on Economic Factors

Consumer Federation of America | Page 18

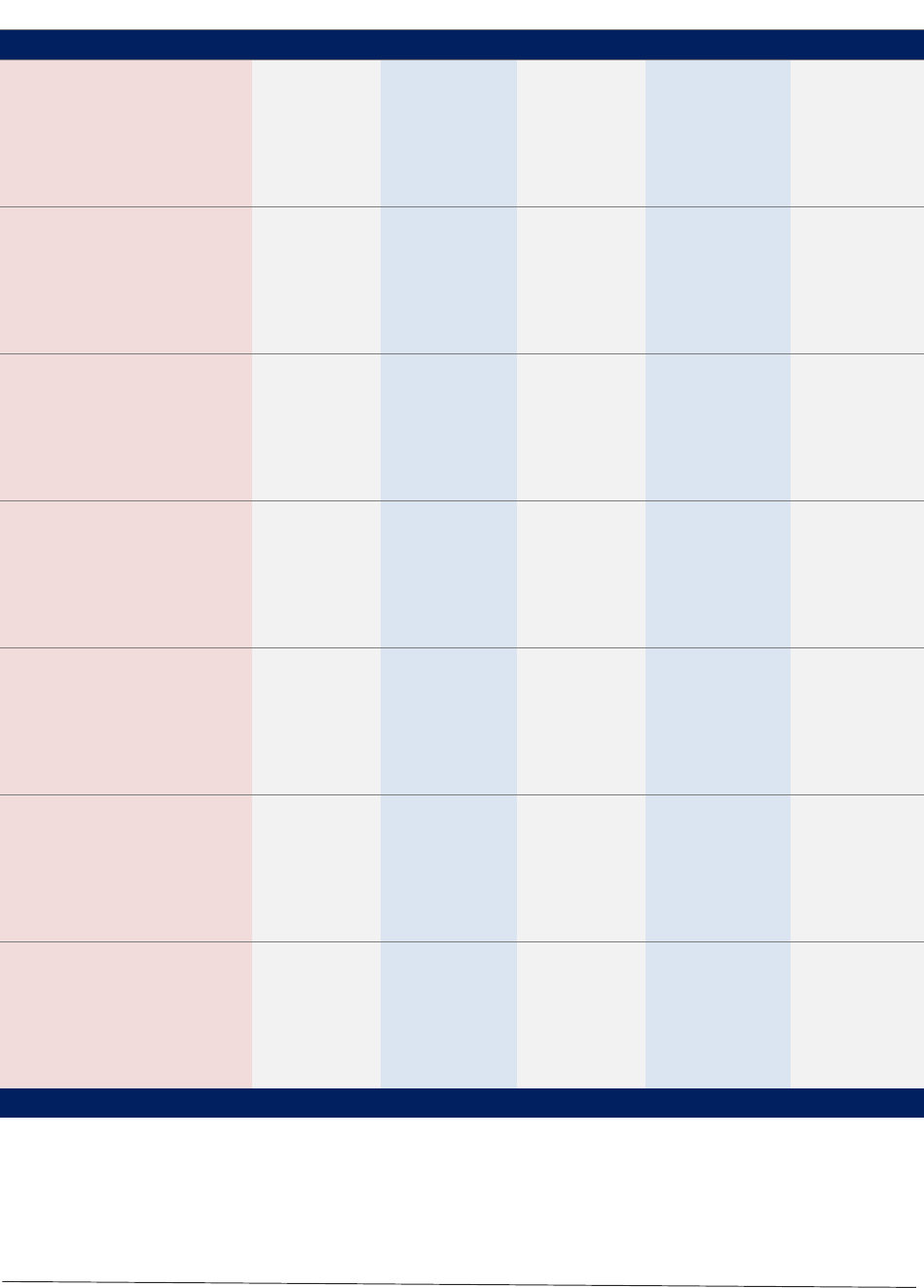

Annual premium by city, driver profile and insurer (con’t)

Kansas City, MO

GEICO

Progressive

Allstate

State Farm

Farmers

High Status Female

$424

$656

$786

$928

$916

Low Status Female

$982

$1,280

N/Q

N/Q

$1,570

High Status Male

$424

$638

$786

$928

$916

Low Status Male

$976

$1,184

N/Q

N/Q

$1,454

Los Angeles, CA

High Status Female

$546

$646

$970

$1,124

$976

Low Status Female

$762

$796

$1,078

$1,124

$976

High Status Male

$546

$716

$970

$1,124

$976

Low Status Male

$732

$760

$1,064

$1,124

$976

Minneapolis, MN

High Status Female

$528

$1,100

$1,946

$994

$3,312

Low Status Female

$2,158

$1,798

$3,342

$994

$4,674

High Status Male

$528

$1,056

$1,946

$994

$2,982

Low Status Male

$1,840

$1,448

$3,070

$994

$3,626

Oklahoma City, OK

High Status Female

$666

$698

$1,252

$976

$692

Low Status Female

$846

$1,194

$1,204

$1,010

$1,394

High Status Male

$666

$684

$1,252

$1,010

$692

Low Status Male

$1,108

$1,140

$1,204

$1,046

$1,404

Phoenix, AZ

High Status Female

$594

$766

$1,278

$746

$1,358

Low Status Female

$1,092

$1,116

N/Q

$772

$2,000

High Status Male

$594

$736

$1,278

$746

$1,282

Low Status Male

$1,126

$998

N/Q

$772

$2,232

Pittsburgh, PA

High Status Female

$544

$522

$1,244

$584

$1,044

Low Status Female

$1,072

$904

$1,378

$606

N/Q

High Status Male

$544

$522

$1,244

$584

$1,044

Low Status Male

$858

$904

$1,378

$606

N/Q

Queens, NY

High Status Female

$1,264

$2,174

$3,350

$2,388

N/A

Low Status Female

$1,566

$6,668

N/Q

$3,974

N/A

High Status Male

$1,264

$1,946

$3,350

$2,438

N/A

Low Status Male

$1,526

$4,734

N/Q

$4,144

N/A

Major Auto Insurers Raise Rates Based on Economic Factors

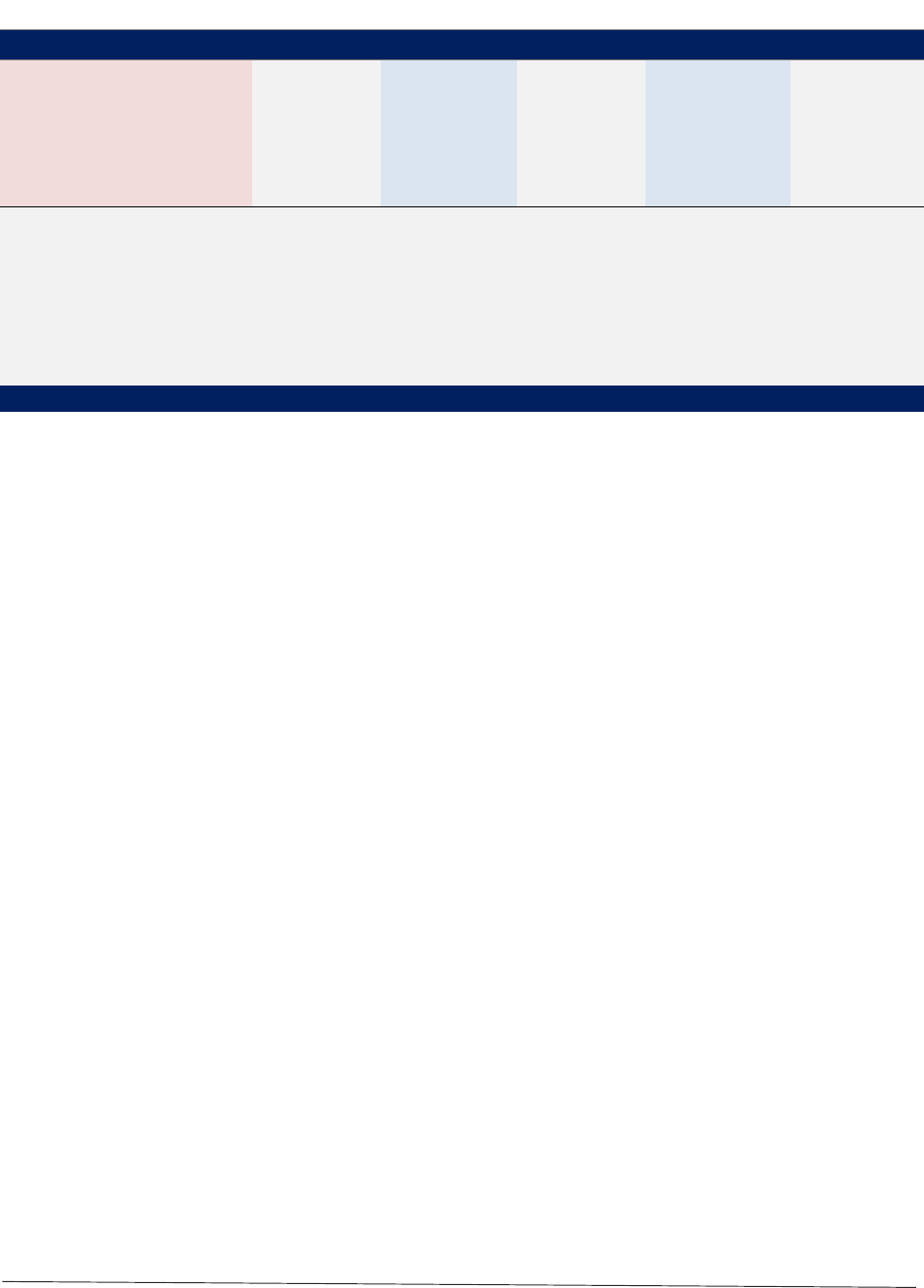

Consumer Federation of America | Page 19

Annual premium by city, driver profile and insurer (con’t)

Seattle, WA

GEICO

Progressive

Allstate

State Farm

Farmers

High Status Female

$730

$972

$1,806

$1,084

$836

Low Status Female

$1,288

$1,780

N/Q

$1,120

$1,736

High Status Male

$680

$686

$1,806

$1,084

$756

Low Status Male

$846

$1,082

N/Q

$1,120

$1,502

Notes

All premiums were provided as six-month quotes and annualized for this report

N/Q: Company did not provide a quote to this driver but does sell policies to drivers in this city

N/A: Company did not provide a quote for any driver

*Allstate-Boston quote includes minimum physical damage coverage because site would not provide a quote for liability

only policies; Allstate-Jersey City quotes are for 50/100 coverage. Company did not provide a minimum limits quote online