ROADMAP FOR FLEXIBILITY SERVICES TO

2030

A report to the Committee on Climate Change

May 2017

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

Contact details

Name

Email

Telephone

Anser Shakoor

anser.shakoor@poyry.com

+44 (0)1865 812 267

Gareth Davies

gareth.davi[email protected]

+44 (0)1865 812 204

Goran Strbac

goran.strbac@imperial.ac.uk

+44 (0)7973 658 976

Copyright © 2017 Pöyry Management Consulting (UK) Ltd

All rights reserved

No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by

any means electronic, mechanical, photocopying, recording or otherwise without the prior written permission

of Pöyry Management Consulting (UK) Ltd (“Pöyry”).

This report is provided to the legal entity identified on the front cover for its internal use only. This report may

not be provided, in whole or in part, to any other party without the prior written permission of an authorised

representative of Pöyry. In such circumstances additional fees may be applicable and the other party may

be required to enter into either a Release and Non-Reliance Agreement or a Reliance Agreement with Pöyry.

Disclaimer

While Pöyry and Imperial college consider that the information and opinions given in this work are sound, all

parties must rely upon their own skill and judgement when making use of it. Pöyry and Imperial college do

not make any representation or warranty, expressed or implied, as to the accuracy or completeness of the

information contained in this report and assumes no responsibility for the accuracy or completeness of such

information. Pöyry and Imperial college will not assume any liability to anyone for any loss or damage arising

out of the provision of this report.

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

Authors

Pöyry Management Consulting

Imperial College London

Anser A Shakoor and Gareth Davies

Goran Strbac, Danny Pudjianto,

Fei Teng, Dimitrios Papadaskalopoulos

and Marko Aunedi

Pöyry Management Consulting

Pöyry is an international consulting and engineering company. We serve clients globally across

the energy and industrial sectors and provide local services in our core markets. We deliver

management consulting and engineering services, underpinned by strong project implementation

capability and expertise. Our focus sectors are power generation, transmission & distribution,

forest industry, chemicals & biorefining, mining & metals, transportation and water. Pöyry has an

extensive local office network employing about 5,000 experts. Pöyry’s net sales in 2016 were

EUR 530 million and the company’s shares are quoted on Nasdaq Helsinki (Pöyry PLC: POY1V).

Pöyry Management Consulting provides leading-edge consulting and advisory services covering

the whole value chain in energy, forest and other process industries. Our energy practice is the

leading provider of strategic, commercial, regulatory and policy advice to Europe's energy

markets. Our energy team of 200 specialists offer unparalleled expertise in the rapidly changing

energy sector.

Imperial College London

The Imperial College team conducted dedicated modelling of the UK’s electricity system for this

report. This team has led the development of novel advanced analysis approaches and

methodologies that have been extensively used to inform industry, governments and regulatory

bodies about the role and value of new technologies and systems in supporting cost effective

evolution to smart low carbon future. The authors would like to express their gratitude to the

Engineering and Physical Sciences Research Council for the support obtained through the Whole

Systems Energy Modelling Consortium and Energy Storage for Low Carbon Grids programmes.

This support enabled the fundamental research that led to the development of modelling

frameworks used in this study.

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

[This page is intentionally blank]

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

TABLE OF CONTENTS

EXECUTIVE SUMMARY 1

1. INTRODUCTION 7

1.1 Overall approach 8

1.2 System flexibility 9

1.3 Flexibility providing technologies 9

1.4 Flexibility services and technologies 10

1.5 Structure of this report 12

1.6 Sources 13

2. MODELLING THE NEED FOR FLEXIBILITY 15

2.1 Modelling assessment of future flexibility requirements 15

2.2 Future flexibility requirements 16

2.3 Impact of alternative generation mixes on flexibility requirements 21

2.4 Potential benefits of alternative system flexibility options 22

2.5 Uncertainties related to the portfolio of flexibility services 24

2.6 Main requirements of the future electricity systems 25

3. ENSURING EFFICIENT FLEXIBILITY INVESTMENT DECISIONS 27

3.1 Availability and accessibility of revenue streams 28

3.2 Efficiency of pricing signals 30

3.3 Improved understanding of long-term requirements 38

4. DEVELOPING CAPABILITY TO MANAGE GREATER COMPLEXITY IN

THE SYSTEM 41

4.1 System operators will need to have clear roles and responsibilities

besides developing capability to manage greater complexity of the

future smart electricity system 41

4.2 Development of energy and smart-enabling infrastructure needs to be

well-coordinated 47

5. ENSURING INNOVATION SUPPORT 49

5.1 Continued support is required to ensure learning in developing

innovative flexibility solutions 49

5.2 Action to ensure innovation 53

6. ENSURING EFFECTIVE CONSUMER PARTICIPATION 55

6.1 Consumers need to be better informed about the benefits that a smart

system offers them 55

6.2 Consumers protection will need to be ensured to build trust for DSR

participation 57

7. SUMMARY OF THE FLEXIBILITY ROADMAP AND INDICATOR

FRAMEWORK 59

7.1 Flexibility roadmap actions 59

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

7.2 Progress monitoring framework 61

ANNEX A – SYSTEM EVOLUTION PATHWAYS TO MEET THE CARBON

INTENSITY TARGETS 65

A.1 Carbon targets 65

A.2 Modelled scenarios 66

A.3 Modelling inputs and assumptions 67

A.4 Overview of the methodology for whole-system analysis of electricity

systems 74

ANNEX B – FLEXIBILITY SERVICES AND TECHNOLOGIES 77

B.1 Flexibility services procured under current arrangements 77

B.2 Mapping flexibility technologies to existing flexibility services 78

ANNEX C – FIRST STAKEHOLDER WORKSHOP 81

C.1 Introduction 81

C.2 Workshop participants 81

ANNEX D – SECOND STAKEHOLDER WORKSHOP 83

D.1 Introduction 83

D.2 Workshop participants 83

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

1

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

EXECUTIVE SUMMARY

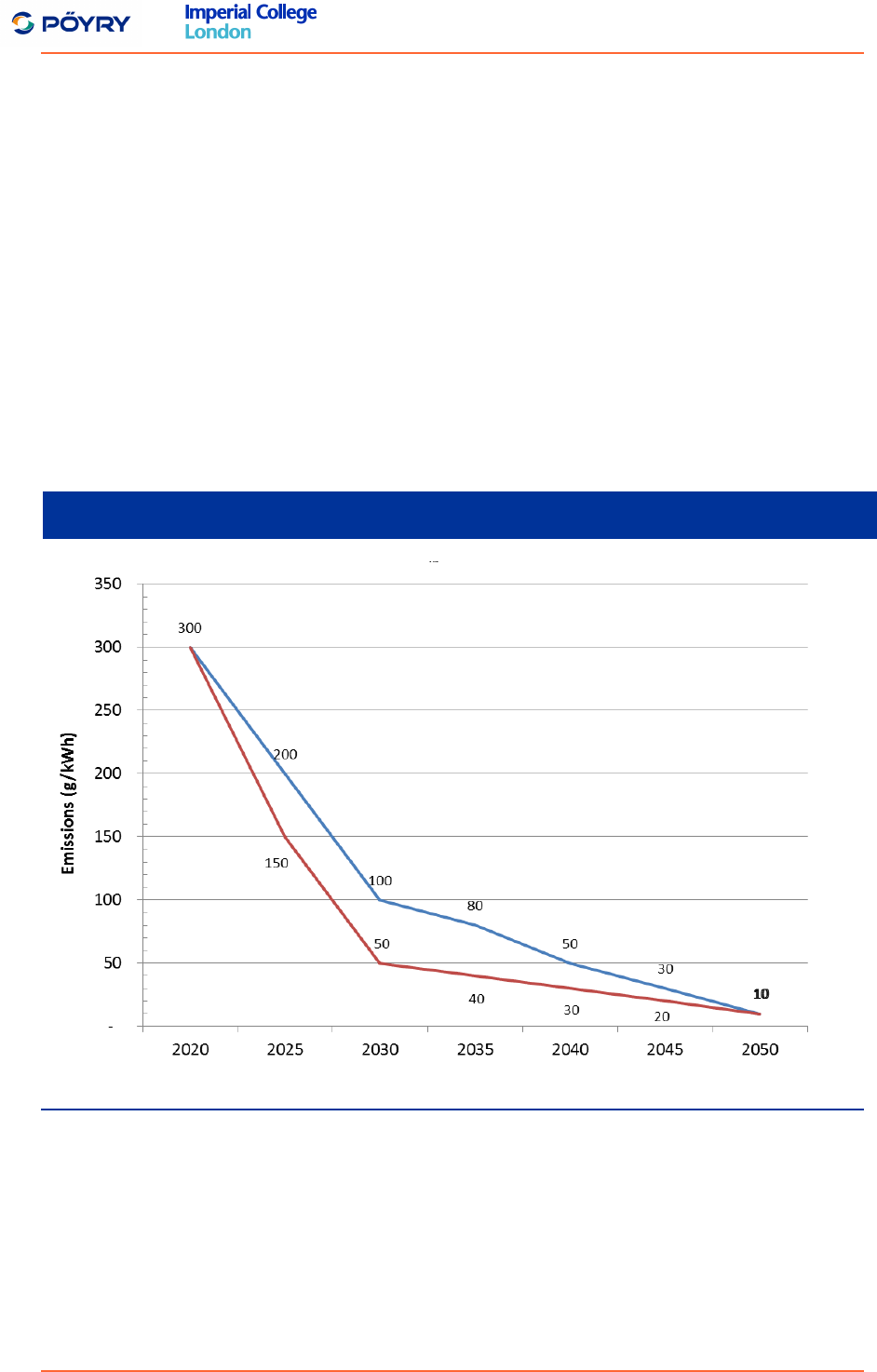

The GB electricity system is expected to undergo a fundamental transformation over the

next few decades in response to tightening energy sector decarbonisation targets. In its

advice to Government on future carbon budgets, the Committee on Climate Change

(CCC) has emphasised the importance of decarbonising the power sector and

recommended that the aim should be to reduce the carbon intensity of power generation

from current levels of around 350 gCO

2

/kWh to around 100 gCO

2

/kWh in 2030.

Delivering on such a target will require investment in a portfolio of low-carbon

technologies and an increase in the provision of flexibility services to enable the cost

effective integration of the new system. Growth in required flexibility will facilitate

development and deployment of innovative technologies and emergence of new business

models and service offerings.

While there are several possible configurations of demand and supply, in any future low-

carbon electricity system we should anticipate:

a much higher penetration of low-carbon generation with a significant increase in

variable renewable sources including wind and solar and demand growth driven by

electrification of segments of heat and transport sectors;

growth in the capacity of distribution connected flexibility resource;

an increased ‘flexibility’ requirement to ensure the system can efficiently maintain

secure and stable operation in a lower carbon system;

opportunities to deploy energy storage facilities at both transmission and distribution

levels; and

an expansion in the provision and use of demand-side response across all sectors of

the economy.

System flexibility, by which we mean the ability to adjust generation or consumption in the

presence of network constraints to maintain a secure system operation for reliable service

to consumers, will be the key enabler of this transformation to a cost-effective low-carbon

electricity system. There are several flexibility resource options available including highly

flexible thermal generation, energy storage, demand side response and cross-border

interconnection to other systems.

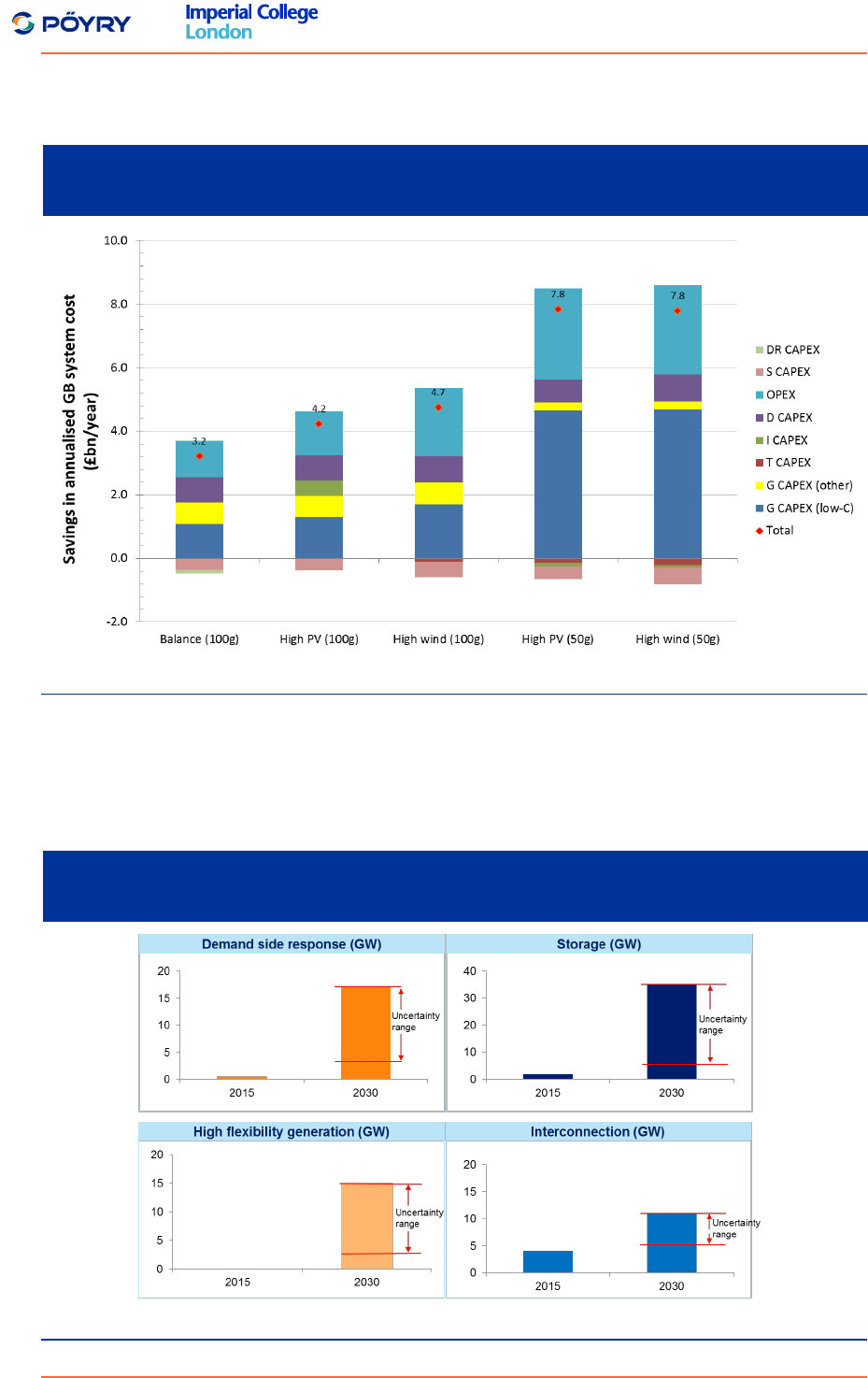

Scenario analysis undertaken by Imperial College as part of this study demonstrates that

the system wide benefits of integrating new sources of flexibility relative to the use of

conventional thermal generation based sources of flexibility, as shown in Figure 1, are

potentially very significant – between £3.2bn and £4.7bn per year in a system meeting a

carbon emissions target of 100gCO

2

/kWh in 2030.

Key categories of system cost savings achievable by accessing the new sources of

flexibility include:

reduced investment in low-carbon generation (between 25% and 60% of the total

savings depending on the scenario), as the available renewable resource and nuclear

generation can be utilised more efficiently enabling the system to reach the carbon

target with less low carbon generation capacity;

reduced system operation cost (between 25% and 40% of the total savings), as

various reserve services are provided by new, cheaper, flexibility sources rather than

by conventional generation; and

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

2

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

reduced requirement for distribution network reinforcement (between 10% and 20% of

the total savings) and backup capacity.

Figure 1 – Potential benefits of efficient integration of new system flexibility

resource

Source: Imperial’s modelling analysis of the CCC scenarios

However, due to uncertainties around future cost and technical performance of different

options, the relative contribution of each flexibility technology may vary greatly, as shown

in Figure 2, and it is therefore important that the future market and regulatory environment

does not distort decisions but delivers clear signals on which participants can base their

investment choices.

Figure 2 – Indication of uncertainty in the deployment of flexibility resource

based on modelling analysis

Source: Imperial’s modelling analysis of the CCC scenarios

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

3

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

From the analysis and stakeholder engagement undertaken as part of this study, we have

identified four key requirements of a future GB electricity system.

Investment decisions should be made on the basis of the full system value

offered by providers – this means that the market design must effectively price and

reward energy, capacity and flexibility.

Appropriate systems and interfaces should be in place to manage greater

complexity in system operation and control – this implies a shift in the resource of

system control from the transmission to the distribution level and a capability of the

system to deal with more interactions between distribution and transmission

networks, and to promote and utilise more active demand management.

Ongoing support for innovation in technology, services and operating models –

it will be important that, as the institutional and market framework evolves, the drive

for innovation across the value chain is not dampened.

Enhanced framework to achieve greater consumer participation – in addition to

establishing the technical infrastructure for demand-side response, legal and

regulatory frameworks around consumer protection and data protection will be

necessary to achieve widespread consumer acceptance.

Flexibility roadmap

To deliver these requirements, action will need to be taken to enhance the market and

regulatory framework and in the course of this study we have developed a roadmap to

facilitate low-carbon flexibility. The roadmap is intended to create a technology neutral

investment environment supported by an innovation programme that facilitates uptake of

the most efficient and cost effective flexibility technologies.

The roadmap, which was informed by a series of stakeholder workshops, defines specific

enabling actions aimed at improving access for flexibility. For each action, we describe

(a) the primary responsible party; (b) the timeframe over which action is required; and (c)

the priority of the action.

Table 1 presents the recommended high priority actions included in the flexibility

roadmap. Lower priority actions, together with a detailed description of the rationale for

the proposed actions and a high-level overview of the relevant ongoing activities is

provided in the main report (Chapter 3 to Chapter 6).

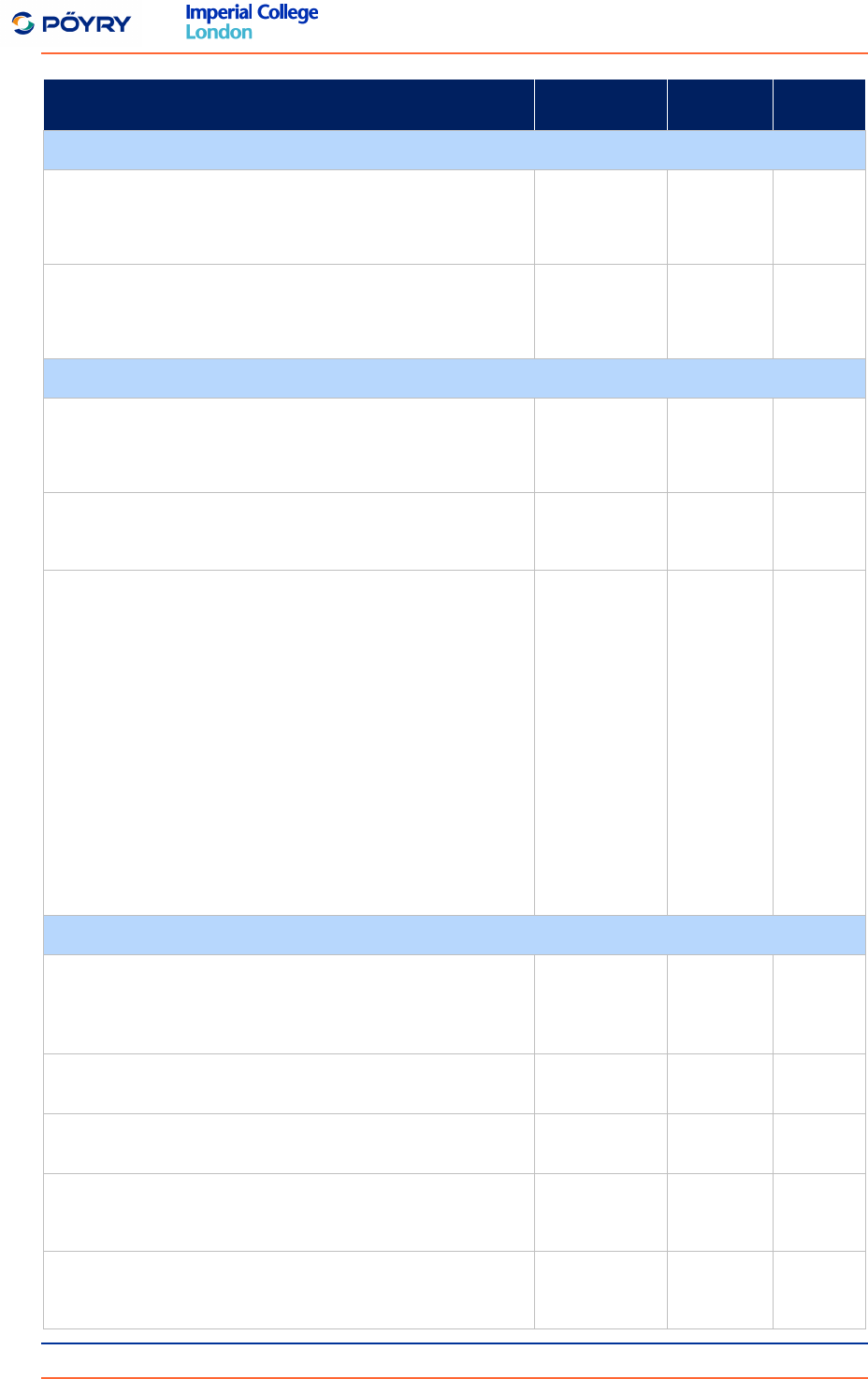

Table 1 – High priority actions of the flexibility roadmap

Action

Responsible

Time

frame

Review characteristics of current procurement processes (e.g.

threshold capacity level to participate, contract terms / obligations)

and the procurement route (e.g. open market, auctioning or

competitive tendering) that enable more efficient procurement of

services without unduly restricting the provision of multiple services

by flexibility providers.

Ofgem in

conjunction

with SO, TOs

and DSOs

By 2020

Assess the materiality of distortions to investment decisions in the

current network charging methodology (e.g. lack of locational

charging, double-charging for stored electricity), and reform charging

methodology where appropriate.

SO, DSOs,

and Ofgem

By 2020

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

4

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

Action

Responsible

Time

frame

Assess the materiality of distortions to investment decisions in the

absence of non-network system integration charging (i.e. back up

capacity and ancillary services) and implement charging where

appropriate.

SO, DSOs,

and Ofgem

By 2020

Publish annual projections (in each year) of longer-term future

procurement requirements across all flexibility services including

indication of the level of uncertainty involved and where possible

location specific requirements, to provide greater visibility over future

demand of flexibility services.

SO and

DSOs

2020

onwards

Publish a strategy for developing the longer-term roles and

responsibilities of system operators (including transitional

arrangements) that incentivises system operators to access all

flexibility resource by making investments and operational decisions

that maximise total system benefits.

Ofgem in

conjunction

with industry

2018

Periodical review of existing system planning and operational

standards for networks and generation, assessing whether they

provide level-playing field to all technologies including active network

management and non-build solutions (e.g. storage and DSR), and

revise these standards as appropriate.

Industry

codes

governance

and Ofgem

Initial

review

by 2019

A number of initiatives led variously by Government, Ofgem, National Grid and wider

industry, are already underway which support our proposed actions. Some of the key

initiatives include:

BEIS and Ofgem’s work on flexibility in 2016 (i.e. BEIS and Ofgem’s position papers

on flexibility) which led to their combined call for evidence for a smart, flexible energy

system. It is a wide scope activity intended to collate stakeholder’s views and

evidence on system flexibility aspects such as; policy and regulatory barriers, price

signals and consumers participation. It also presents alternative future models for

system and network operator roles and responsibilities for stakeholder feedback.

Power Responsive is a stakeholder-led programme, facilitated by National Grid, to

stimulate increased participation in the different forms of flexible technology such as

DSR and storage. National Grid is also working on rationalising the portfolio of the

flexibility services it procures.

The network companies have initiated a case to carry out a thorough review of

Engineering Recommendation (ER P2) for the planning of distribution networks.

Ofgem has supported this initiative as well as the public engagement process

assessing the P2 review on the design of the electricity distribution networks and

changes to SQSS (GRS 022) in relation to the integration of new technologies in the

networks.

The combination of the ongoing work and the proposed roadmap actions will create a

more robust and supportive environment for efficiently meeting the future flexibility

requirements in the system.

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

5

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

Progress monitoring framework

In order to monitor progress in development of low-carbon flexibility, we have developed

indicators that can be used by the CCC. The indicators and monitoring framework serve

the following two main purposes:

monitor whether the proposed actions are being implemented in line with the

roadmap; and

to assess the impact of actions – i.e. actual progress in the market around

assimilating ‘smart’ flexible solutions.

Performance against specific actions

In relation to specific actions recommended in the roadmap we have, where appropriate,

defined a time frame for completion of the action. Where actions are ongoing, this is

noted separately.

Any delay in the completion of actions will need investigation to understand the reasons

for such delay and its knock-on effect (if any) on other actions and wider achievement of

decarbonisation objectives.

For the ongoing actions, a periodical monitoring will be required to check that progress is

in line with the requirements and objectives set out in the roadmap.

Performance of the market in general

Performance in this area will be linked to the assessment of measureable impacts of

actions on delivering enhanced and efficient volumes of flexibility in the GB system.

However, the challenge with developing any quantitative metrics is that there is no precise

target for particular forms of flexibility provision. This is driven by the uncertainties around

costs and technical development of different types of flexibility sources as well as the

long-term evolution of supply mix and market and regulatory frameworks.

In the above context and considering the practicality of collecting and processing

information to determine an indicator, we propose that a broad measure of the

deployment of additional capacity of flexible technologies should be used as the key

indicator to measure the impact of roadmap action.

Based on the modelling analysis undertaken as part of this study for alternative future

generation scenarios, we have assessed the required range of additional capacity of

different flexible technologies to efficiently meet 2030 carbon intensity targets. Figure 3

shows these additional capacity requirements based on the modelling analysis

undertaken as part of this study. The low and high levels for a given flexibility technology

are based on its range of penetration across the four main future scenarios investigated in

this study (see Section A.2 for scenario details) whereas the central level shows the mid-

point of the range.

The central levels of additional capacity of flexible technologies are to be used to track

progress on deployment of technologies in a given period. It is expected that a trade-off

between various technologies will also take place. For example, lower deployment of

additional storage may be compensated by higher uptake of another technology thus

meeting the system’s overall flexibility requirements.

However, a consistent low deployment of one or more technologies across several years

could be seen as a flag for further investigation – e.g. to identify if there is a specific

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

6

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

barrier that is hindering the deployment of the technology or affecting its competitiveness

against other flexibility technologies.

Figure 3 – Potential levels of flexibility providing capacity (GW)

Source: Imperial’s modelling analysis

Considering the value and scalability of DSR we also propose that the following two

indicators should be used to assess the progress for this particular flexibility resource:

growth in number and size (i.e. total contracted volume, MW) of aggregators

providing DSR-based flexibility in the market; and

growth in the share of smart appliances as a percentage of total appliances sold each

year.

Low Central High Low Central High Low Central High

New flexible generation 1 3 5 2 6 10 3 9 15

Storage 0.8 2.9 5 3.2 11.6 20 5.6 20.3 35

DSR 2.1 6.3 10.5 2.76 8.28 13.8 3.42 10.26 17.1

Interconnection 3.4 3.4 3.4 4.45 5.825 7.2 5.5 8.25 11

By 2030

Flexible technology

By 2020

By 2025

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

7

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

1. INTRODUCTION

The GB electricity system is expected to undergo a fundamental transformation over the

next few decades in response to tightening energy sector decarbonisation targets,

development and deployment of innovative technologies and emergence of new business

models and service offerings. While there are several possible configurations of future

demand and supply, we should anticipate:

a much higher penetration of low-carbon generation with a significant increase in

variable renewable sources including wind and solar;

an increased ‘flexibility’ requirement to ensure the system can efficiently maintain

secure and stable operation;

growth in the capacity of distribution connected flexibility resource;

opportunities to deploy energy storage facilities at both transmission and distribution

levels; and

an expansion in the provision and use of demand-side response across all sectors of

the economy.

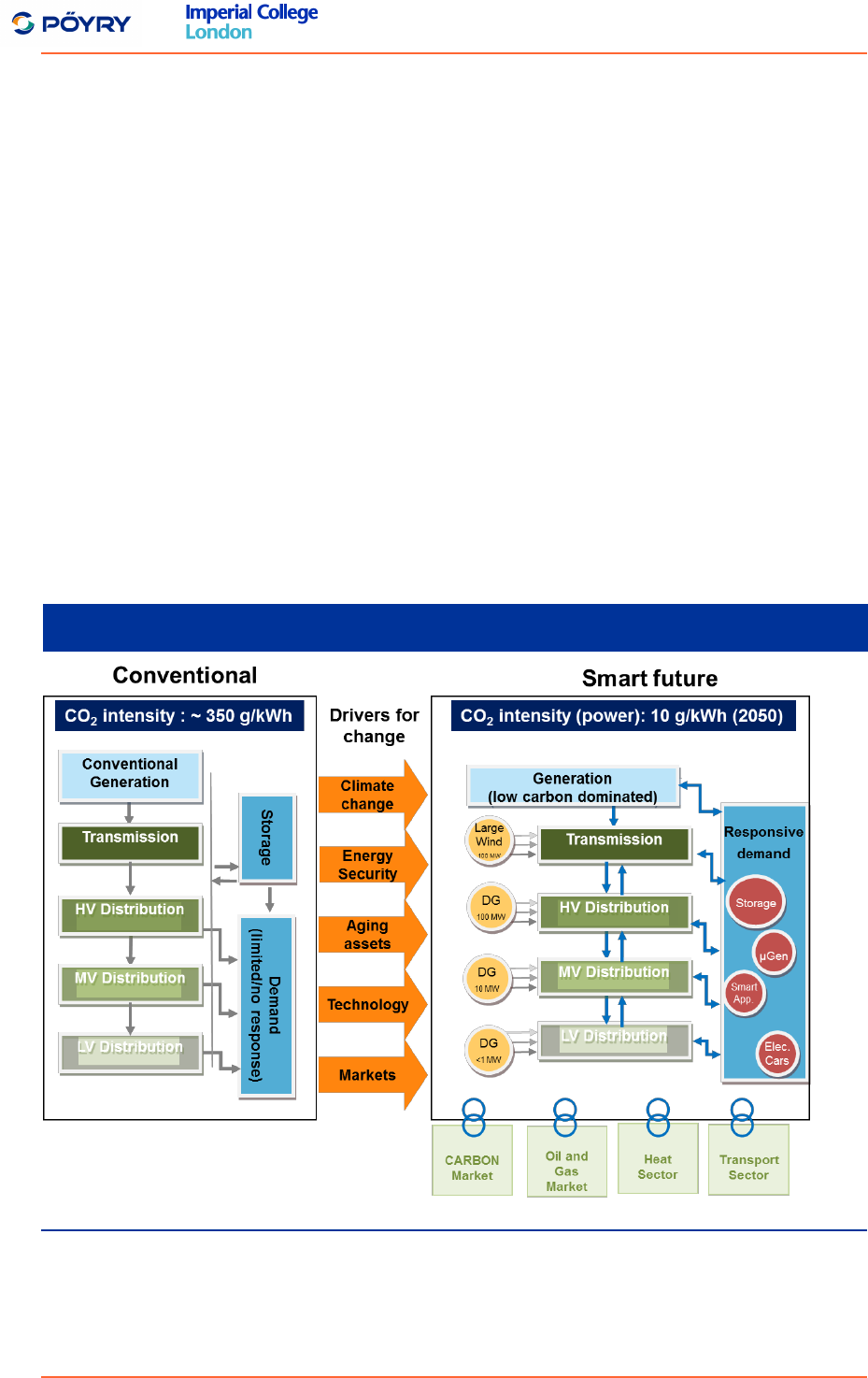

This paradigm shift in the GB electricity system is depicted in Figure 4 below.

Figure 4 – Potential evolution of power system in GB

Source: Imperial College

System flexibility will be the key enabler in delivering this transformation. It is important

not only in the context of maintaining secure and efficient system operation but also for

maximising the utilisation of the assets thus reducing the need for investment in new

generation and network capacity. However, the volume of increased flexibility in the

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

8

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

system is uncertain, and how and through which technologies these additional flexibility

requirements will be served is also not clear.

The Committee on Climate Change, therefore, is looking to develop a roadmap for

flexibility services out to 2030. The Committee have engaged Pöyry and Imperial College

to develop the roadmap for the provision of flexibility services that would facilitate meeting

the CO

2

emission reduction target of below 100gCO

2

/kWh for the UK electricity sector by

2030.

1.1 Overall approach

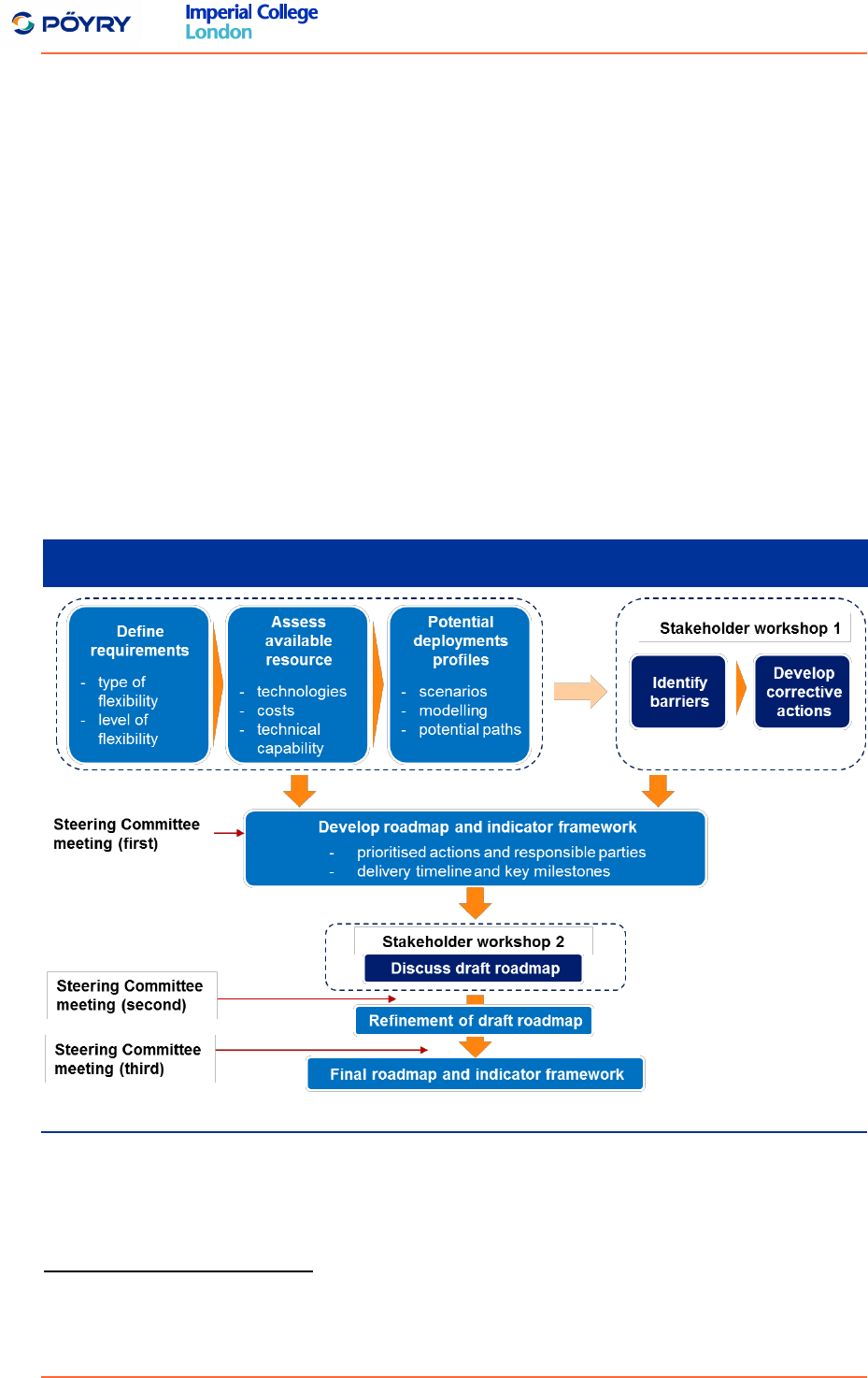

In order to develop the roadmap we have applied the approach shown in Figure 5. Our

approach includes research, review and analysis of the flexibility landscape (required

flexibility services, flexibility providing technologies and relevant procurement processes),

primarily focused on Great Britain and supplemented by knowledge and understanding of

the same issues in other systems. Furthermore, a detailed quantitative assessment of the

CCC scenarios

1

was also carried out by Imperial College to evaluate future flexibility

requirements under alternative generation and demand projections of the GB electricity

system.

Figure 5 – Roadmap development approach

1

Power sector scenarios for the fifth carbon budget, The Committee on Climate Change (UK),

October 2015

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

9

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

In addition to Pöyry and Imperial’s research and analysis, the project also benefitted from

stakeholder input through two workshops:

Stakeholder Workshop 1 was focused on identifying the barriers to deployment of

different types of flexibility options and developing ideas on actions to address these

barriers.

Stakeholder Workshop 2 tested the draft flexibility roadmap with stakeholders by

presenting the future flexibility requirements and discussing the actions for facilitating

provision of enhanced flexibility out to 2030.

The list of participating organisations and their representatives in the first and second

workshops are provided in Annex C and Annex D respectively.

The project work and findings were overseen by a Steering Committee comprising

members from the Committee on Climate Change, BEIS and Ofgem. The project Steering

Committee provided highly valuable feedback and guidance during three meetings at key

milestones during the project.

While stakeholder and Steering Committee inputs have greatly contributed to the

development of the roadmap, we (Pöyry and Imperial) have maintained our independent

analysis in defining the actions necessary to enable an efficient provision of flexibility in

the future GB electricity system.

We acknowledge that a number of enabling activities are already being progressed by

Government, Ofgem, National Grid and the wider industry. Our proposed actions are

intended to build upon or complement these ongoing activities and they are explicitly

referred to in the relevant sections of the report.

1.2 System flexibility

In this report system flexibility is defined as the ability to adjust generation or consumption

in the presence of network constraints to maintain a secure system operation for reliable

service to consumers. It has the following two components:

Operational flexibility – i.e. the use of resources, both energy and ancillary services,

to ensure efficient and secure system operation; and

System adequacy – i.e. maintaining the long-term capacity requirement of the

system.

The two forms of flexibility are complementary to each – for example, the energy storage

supports maintaining demand-supply balance during system operation and it can also

reduce system’s peak demand lowering the need for generation and network capacity in

the long-term. Imperial’s modelling based assessments presented in this report take

account of the synergies and complementarities between the two forms of flexibility as

well as across different flexibility providing technologies.

1.3 Flexibility providing technologies

In response to the flexibility challenge, novel flexible technologies that can make more

efficient use of the existing infrastructure are emerging.

The analysis in this report focused on the following types of flexibility providing

technologies.

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

10

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

Flexible generation: advances in conventional generation technologies are allowing

them to provide enhanced flexibility to the system. This is due to their ability to start

more quickly, operate at lower levels of power output (minimum stable generation),

and achieve faster changes in output (see Table 5 for technical parameters of flexible

generation as applied in our modelling work).

Cross-border interconnection: interconnectors to other systems enable large-scale

sharing of energy, ancillary service and back-up resources.

Demand Side Response (DSR): DSR schemes can re-distribute consumption and

engage demand-side resources for system balancing to enhance system flexibility

without compromising the service quality delivered to end customers. These

schemes have a significant potential to provide different types of flexibility services

across multiple time frames and system sectors, from providing primary frequency

response to facilitating network congestion management.

Energy storage: energy storage technologies have the ability to act as both demand

and generation sources. They can contribute substantially to services such as

system balancing, various ancillary services and network management.

In addition to the above mentioned flexibility providing technologies, there is significant

potential for the power sector to access the flexibility embedded in other energy sectors

particularly the heat and gas sectors. However, understanding the effectiveness and

implications of exploiting this flexibility resource needs further research and analysis. This

flexibility resource is discussed further in Section 5.1.3.

1.4 Flexibility services and technologies

In order to ensure that generation and demand are balanced at all times and in all

locations, GB System Operator (i.e. National Grid) employs a range of measures (i.e.

Flexibility Services) across various time horizons. These services are secured under

various procurement mechanisms (e.g. markets, bilateral agreements, competitive

tendering, etc.) and can be broadly broken down as follows:

Capacity market: the aim of the Capacity Market (CM) is to deliver generation

adequacy. Capacity contracts are allocated to providers through auctions intended to

secure a capacity requirement in order to meet the reliability standard set by the UK

government.

Wholesale energy market: this market allows generators to sell their electricity to

suppliers from several years ahead up until Gate Closure.

2

Balancing Market (energy): its purpose is to maintain demand and supply balance

post Gate Closure as Generators and suppliers will most likely generate or consume

more or less than they have sold or bought in the Wholesale market. The System

Operator accepts offers and bids for electricity to enable it to balance the

transmission system during the post Gate Closure period.

Ancillary (Balancing) services: these are used by the System Operator to ensure that

supply meets demand at all times and that the system frequency remains within

statutory limits around the target level of 50Hz. Main balancing services are:

Short Term Operating Reserve (STOR) – to retain spare generation capacity (or

demand reduction) on stand-by during certain hours of the day (typically during

2

Gate Closure is the time by which all notifications must be given; currently it is set at 1 hour

prior to the start of the traded period.

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

11

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

periods of rapid change in demand or generator loading) for dealing with actual

demand being greater than forecast demand and/or plant unavailability.

Fast Reserve – provides a rapid and reliable delivery of active power through an

increased output from generation or a demand reduction, following receipt of an

electronic despatch instruction from National Grid. This service operates in

quicker timeframes than STOR.

Frequency Response – is the automatic provision of increased/reduced

generation or demand reduction/increase in response to a drop or increase in

system frequency. It can be delivered through either Dynamic Response (a

continuous service used to manage second by second changes on the system)

or Static Response (a discrete service usually triggered by a defined frequency

deviation).

Enhanced Frequency Response – achieves 100% active power output at 1

second (or less) of registering a frequency deviation. This is a new service that is

being developed to improve management of the system frequency pre-fault, i.e.

to maintain the system frequency closer to 50Hz under normal operation.

In addition to the above mentioned main flexibility services, a range of other services are

also used by the System Operator which are defined in Annex B.

A number of technologies are capable of providing the various types of flexibility services

required in the system. Table 2 summarises technologies which are currently providing

the key flexibility services in the GB electricity systems (see green dots) and those that

are technically capable of providing the services based on their existing technical

characteristics or with some technical improvements (see red dots). The lack of current

service provision may be for several reasons including commercial constraints, market

limitations or lack of incentives. For example, DSR can provide Enhanced Frequency

Response (EFR) but no DSR aggregator was successful in securing a contract in the

recent EFR auctions because bids were out of merit.

It is also worth noting that in some cases, although a technology is providing a given

service, its market share for the service could be very small. For example, wind

generation provided only 0.03% of total frequency response (FR) in 2015. It could

potentially provide significant volumes of additional FR in the form of synthetic inertia if

appropriate regulatory requirements or incentives were in place and this was considered

efficient.

Therefore, there is a need for: (a) innovation support to improve technical characteristics

of such technologies; and (b) improvements in existing flexibility markets, including

procurement processes, in order to enable and facilitate access of such technologies in

providing a wider range of flexibility services.

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

12

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

Table 2 – Flexibility services and technologies

Source: Pöyry analysis

1.5 Structure of this report

The rest of this report is organised as follows:

Chapter 2 provides the findings of the modelling analysis carried out as part of this

study. It highlights the higher flexibility demands in the future system and identifies

portfolios of technologies to meet this.

Chapter 3 to Chapter 6 provide our analysis on each of the four identified components

of an effective low-carbon flexibility system:

ensure efficient investment decisions in providing increased flexibility services;

develop capability to manage greater complexity in future smart electricity

systems;

ensure innovation support; and

ensure effective consumer participation for exploiting demand flexibility potential.

and the actions required to achieve them.

Chapter 7 summarises the roadmap actions and describes the progress monitoring

framework.

There are four annexes to the report.

Annex A contains key modelling assumptions and methodology as applied by

Imperial College in quantifying the need and benefits of system flexibility.

STOR

FAST

reserve

Frequency

response

Enhanced

Frequency

Response

Coal

• • • •

Nuclear

• • • •

Gas-CCGT

• • • • • •

Gas-OCGT

• • • • • •

CHP (Thermal / RES)

• • • • • •

Biomass

• • • • • •

Engines (gas / diesel)

• • • • •

Wind (onshore / offshore)

• • • • • •

Solar - PV

• • • •

Solar - CSP

• • • • • •

Hydro (reservoir)

• • • • • •

Marine (wave, tidal, etc.)

• • • • • •

Hydro (pump storage)

• • • • • •

Storage (batteries)

• • • • • • •

Demand Side response

• • • • • • •

• Technology is able to provide and is currently providing the relevant service

Blank cells indicate absence of any evidence or information to map technologies onto flexibility services

• Technology that can potentially provide the service but is currently restricted due to economic or market limitations, or

requires some technical improvements for providing the releavnt service

Main balancing services

Wholesale

energy

market

Capacity

market

Balancing

market

(Energy)

Technology

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

13

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

Annex B provides an overview of the flexibility services currently procured by the

system operator, and mapping of flexible technologies to various flexibility services in

the future.

Annex C and Annex D list the participants who joined the two stakeholder

workshops.

1.6 Sources

Unless otherwise attributed the source for all tables, figures and charts presented in this

report is Pöyry Management Consulting.

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

14

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

[This page is intentionally blank]

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

15

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

2. MODELLING THE NEED FOR FLEXIBILITY

System flexibility will be the key enabler for an efficient transformation to the future smart

electricity system. There is a general acknowledgement that a low-carbon power sector

will need greater system flexibility to maintain stable and secure operation because of the

nature of the generation technologies. However, the scale of growth and the mix of

flexibility services required will depend on the way in which the decarbonisation of the

power sector is achieved.

2.1 Modelling assessment of future flexibility requirements

As part of this study, a detailed modelling based assessment was carried out by Imperial

College to investigate how flexibility requirements change in a system that meets the CO

2

emissions intensity target for the power sector (i.e. 100gCO

2

/kWh by 2030 and

10gCO

2

/kWh by 2050). The modelling investigated how flexibility needs changed across

four alternative future scenarios of low-carbon generation.

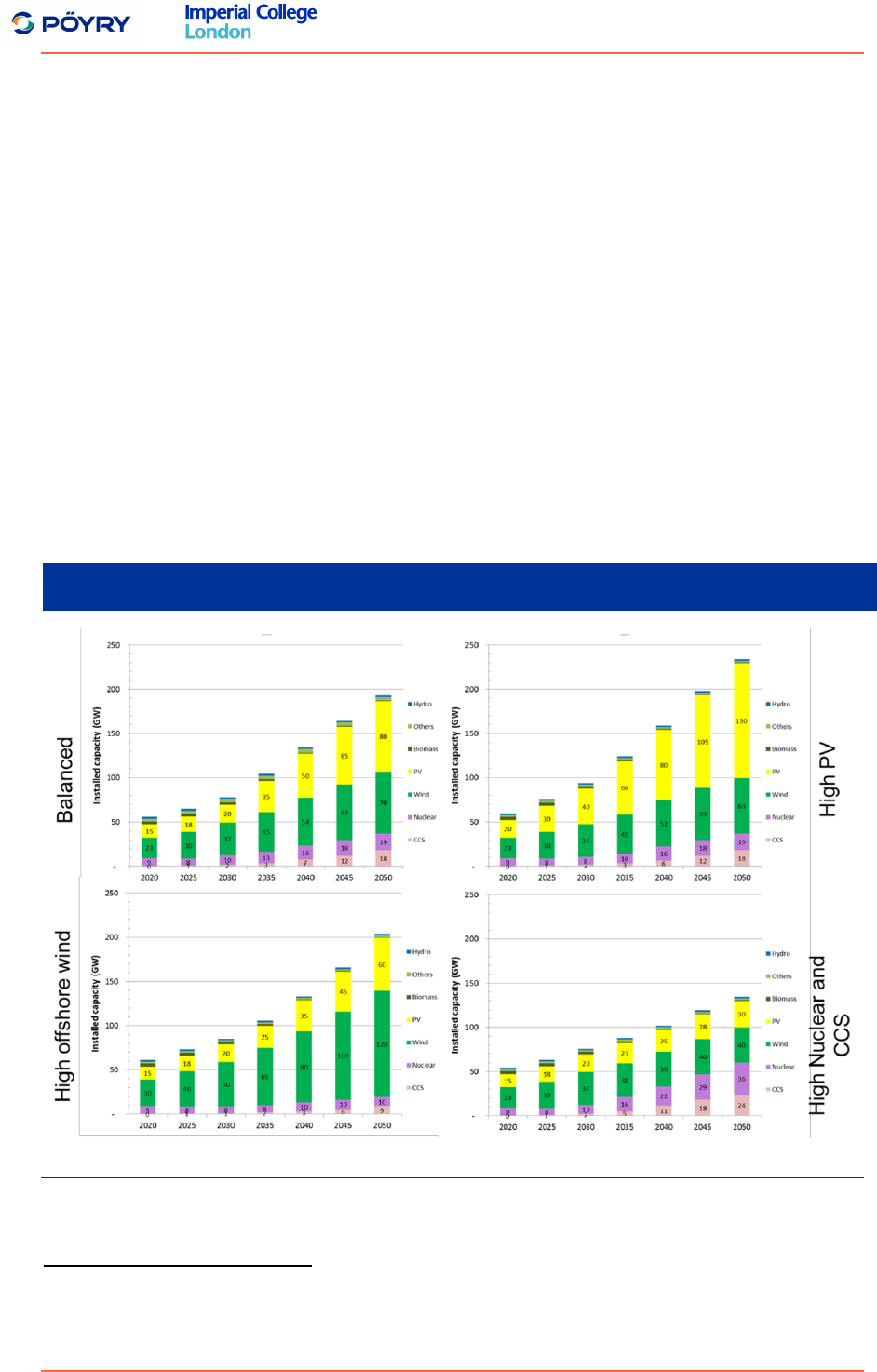

Balanced scenario: assumes balanced development across different low-carbon

technologies (i.e. nuclear, CCS and renewables). The scenario is based on the

extrapolation of the CCC power sector scenarios.

3

High PV scenario: assumes a large deployment of PV which significantly exceeds

the development of other low-carbon technologies. This would be facilitated by a

rapid decrease in the cost of solar cells, massive technology development in this

area, and incentives given to the PV industry to stimulate significant growth.

High offshore wind scenario: as the UK has one of the best wind sources in the

world, this scenario reflects extensive exploitation of this large energy potential for

decarbonisation of the UK electricity industry.

High nuclear and CCS scenario: assumes that the future decarbonisation of the

system will depend on the energy production primarily from nuclear and CCS.

The modelling provides a range of insights into the challenges of managing a low-carbon

generation system and the potential benefits from access to a wider set of flexibility

providers and technologies. In particular, it highlights that:

regardless of the composition of the future energy mix, any low-carbon system will

have a materially higher demand for system flexibility;

because of the different technical characteristics of the low-carbon generation

technologies, the balance of additional flexibility services can be very different to

today;

flexibility can be provided by a variety of new sources (including DSR, energy storage

and additional interconnection) and deliver savings compared to relying on

conventional sources of flexibility (e.g. conventional thermal plants like combined

cycle gas turbines or open cycle gas turbines);

savings can be made in investment and operating costs across the value chain

if decisions are based on the full system value; and

3

Power sector scenarios for the fifth carbon budget, The Committee on Climate Change (UK),

October 2015

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

16

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

the future flexibility portfolio is uncertain and will need to be responsive to a

range of external factors including policy and market initiatives, technology costs

and efficiency improvements.

These insights have helped inform the focus of actions in the flexibility roadmap.

Importantly, they have demonstrated the need for any future market to encourage access

from as wide a set of flexibility resource as possible, and not to be unduly restrictive given

the various uncertainties around new technologies. In addition, they have emphasised the

importance of continued support for innovation and clear, transparent signals of value for

all flexibility services.

The remainder of this Chapter presents the key modelling insights in each area. An

overview of the modelling methodology applied by Imperial College in this analysis and

the key modelling assumptions are provided in Annex A.

2.2 Future flexibility requirements

Any future low-carbon power system will potentially have a large penetration of

intermittent generation, or less flexible nuclear / CCS plants, or a combination of these low

carbon sources. This generation setup drives the need for significant additional flexibility

over shorter time scales (i.e. between few hours ahead to the real-time) necessary to

maintain safe and efficient operation of the system as described in the following sections.

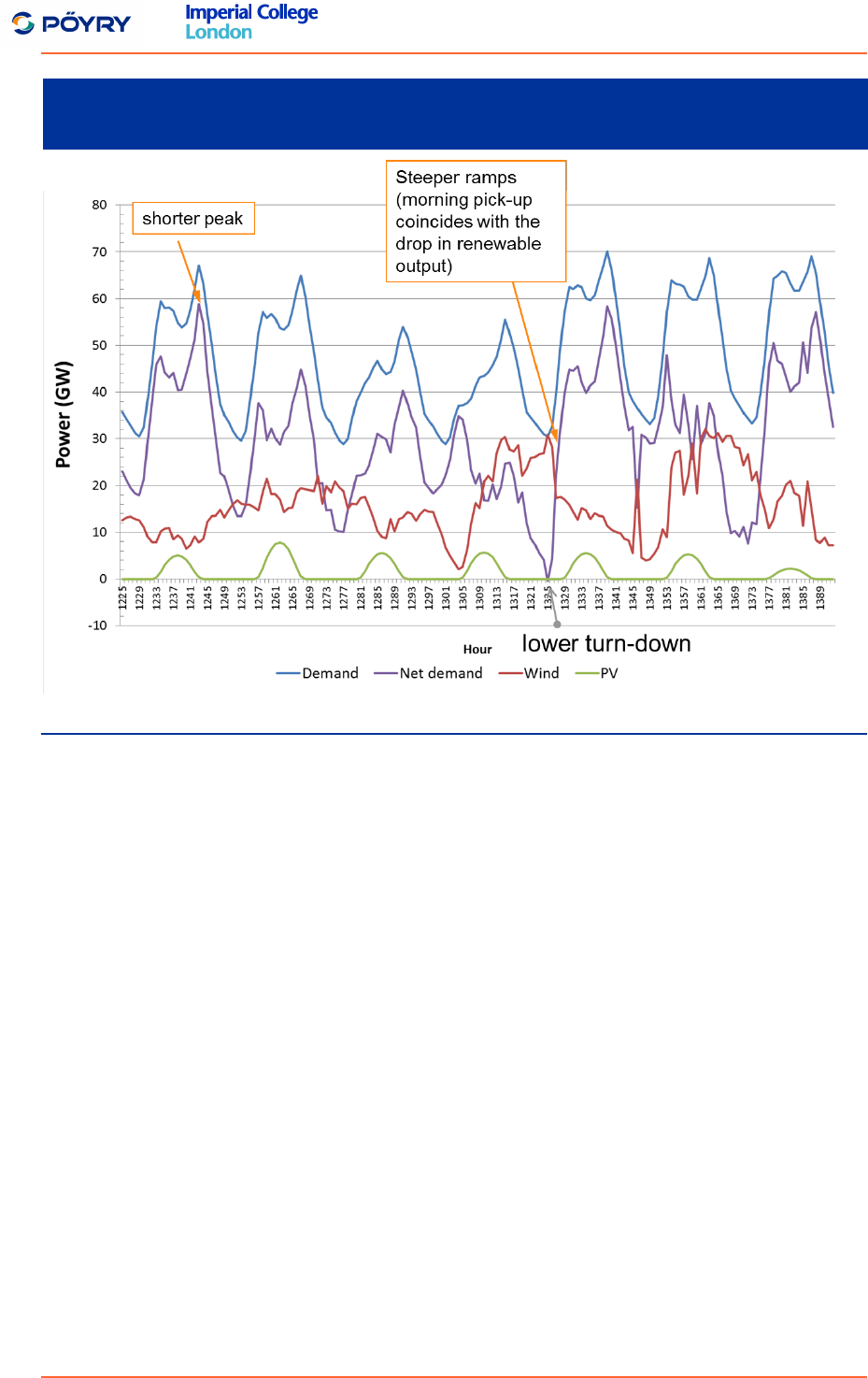

Figure 6 shows an illustrative

4

snapshot of the hourly net demand profile (i.e. system

demand minus intermittent generation) in a single winter week in 2030. A key observation

is that the net demand turns more volatile and often peakier with shorter duration of peak

demand in the future than today. This leads to a need for a very steep ramping

requirement – i.e. increase as well as decrease in generation or demand from

dispatchable resources (demand or generation) in the system.

In this case, the steepest ramp requirement is found when the morning pick-up coincides

with a large drop of renewable output. For safe operation of the system, a large number

of dispatchable generators will need to be synchronised to be able to meet this ramping

requirement in order to maintain demand-supply balance in the system.

Figure 6 also shows that the minimum net demand levels which occur during a low

demand period coincide with high renewable output. The minimum net demand

approaches zero indicating that the entire system demand is supplied by renewables

during such periods. However, such conditions create a challenge in power system

operation since renewables such as wind and solar PV do not contribute to the system

inertia and are not the main providers of frequency response or regulation.

In order to mitigate the risk to safe operation of the system, a sufficient number of

conventional plants need to be synchronised operating at least at the minimum stable

generation level. This will lead to surplus generation in the system resulting in curtailment

of renewable generation unless demand can be increased or energy is exported to other

systems in order to accommodate the surplus energy.

4

The week is drawn from the modelled scenarios to demonstrate the potential volatility in net

demand to be managed by the system operator through its range of flexibility services.

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

17

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

Figure 6 – An illustrative example indicating higher requirement for operational

flexibility in the future (Balanced scenario)

Source: Imperial’s modelling analysis

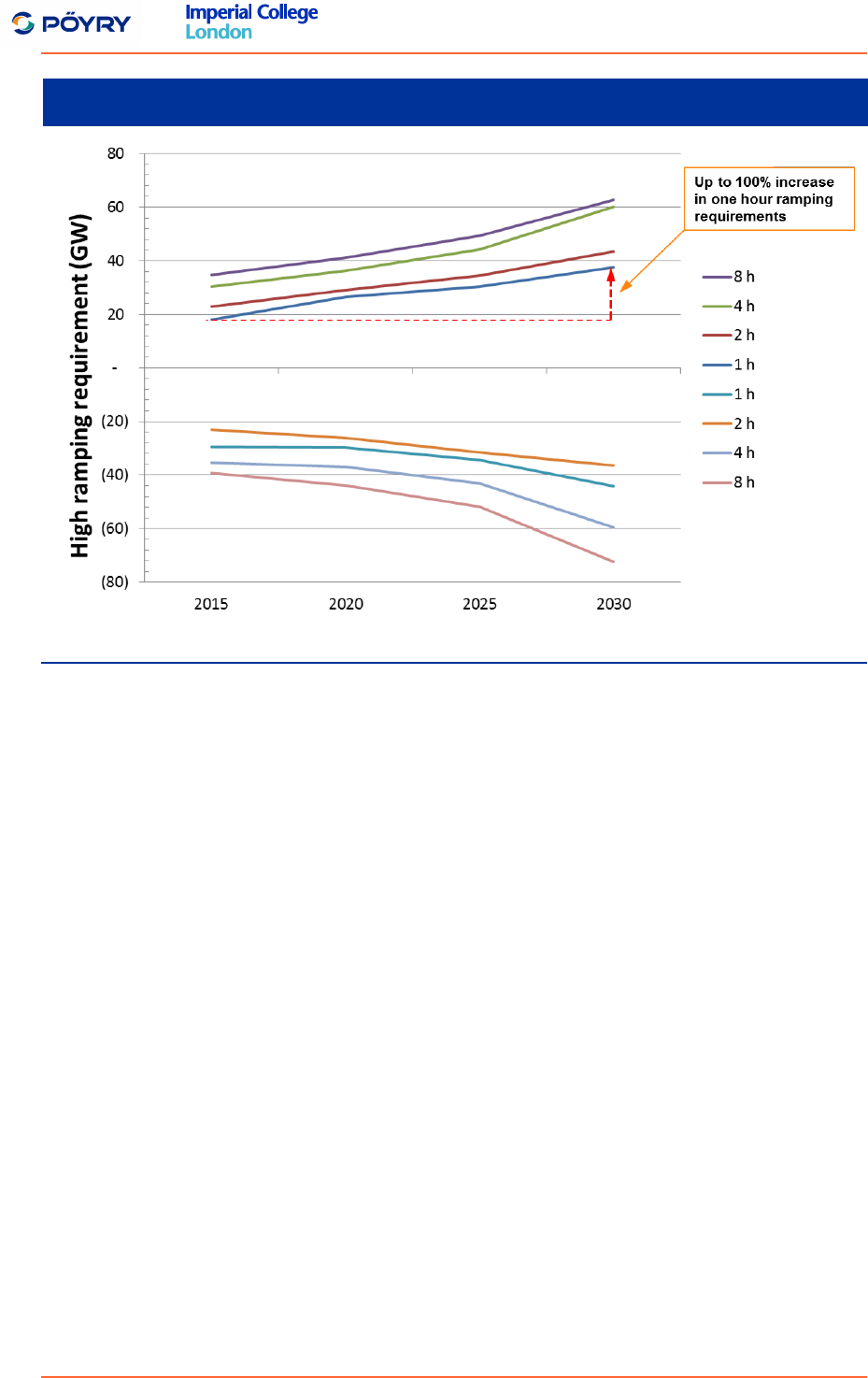

2.2.1.1 Ramping requirements

Based on the modelling of scenarios analysed in this study, it is estimated that there will

be an increase of up to 100% in the maximum ramping requirements over a one-hour time

horizon in 2030 relative to the current situation. This is primarily driven by the increased

renewable energy capacity. The maximum ramping up and ramping down requirements

for different time scales (1 up to 8 hours) are shown in Figure 7.

In general, the ramping requirements increase over all time horizons (i.e. across 1-8

hours). This requires the system operator to plan a larger volume of ramping capability of

the synchronised generators or other dispatchable demand/supply resource in the system

within the respective time frame to meet the demand-supply balancing challenge.

Meeting the increased ramping requirements by fossil based generation is expensive due

to (a) efficiency losses as some plants will be required to run part-loaded; (b) increased

number of start-ups; and c) increase in CO

2

emissions driven by efficiency losses. On the

other hand, lack of adequate ramping capability in the system can jeopardise the safe

operation of the system and potentially increases the need and cost of other (more

expensive) flexibility services by several folds that are required over shorter term frames.

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

18

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

Figure 7 – Increase in ramping requirement (Balanced scenario)

Source: Imperial’s modelling analysis

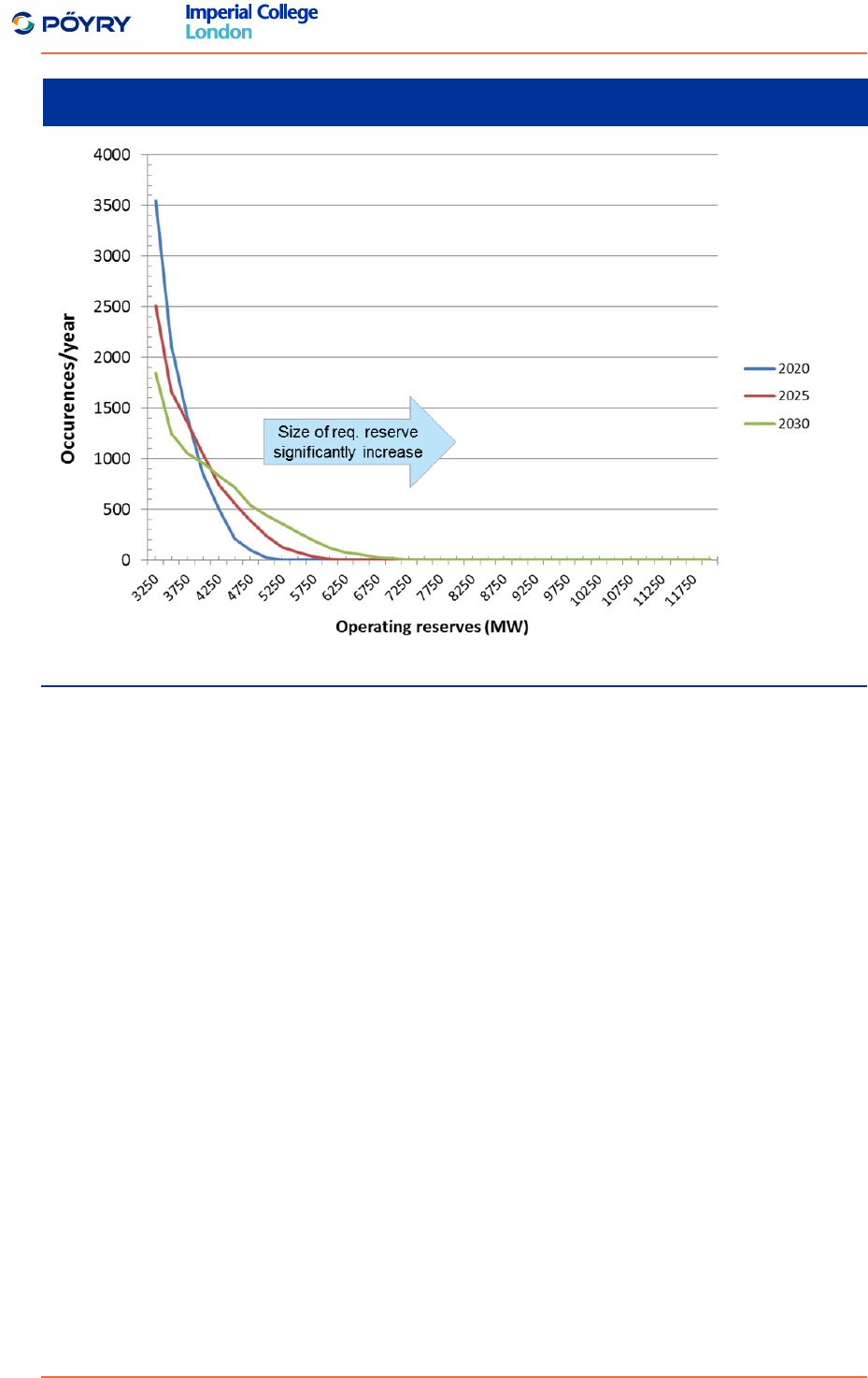

2.2.1.2 Reserve requirements

Operating reserve includes the provision of increased generation or demand reduction

over a period of minutes to hours in response to an instruction from the system operator.

Increased share of variable intermittent generation in the system also increases the

uncertainty in demand and supply balance which increases the minimum operating

reserves held by the SO to maintain sufficient system balancing capability. The amount of

operating reserves depends on the level of uncertainty in supply and demand; so it is

assessed dynamically and changed according the system conditions.

Figure 8 shows two implications of the low-carbon system:

a) a higher maximum requirement – e.g. the maximum reserve requirement across the

year increase from 5.2 GW in 2020 to 7.3 GW in 2030; and

b) a more frequent need of higher reserve levels – e.g. the number of hours during

which a reserve volume of 4.5GW will be required increase from about 300 in 2020

to 700 in 2030.

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

19

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

Figure 8 – Future GB operating reserves requirement (Balanced scenario)

Source: Imperial’s modelling analysis

Today, the operating reserves mainly come from mid-merit (Combined Cycle Gas Turbine

plants and Coal plants) and peaking plants (Open Cycle Gas Turbine). The available

capacity of these technologies is expected to decrease in future in line with tighter

decarbonisation targets and reduced economic viability. Therefore, the system will need

to source alternative operating reserves.

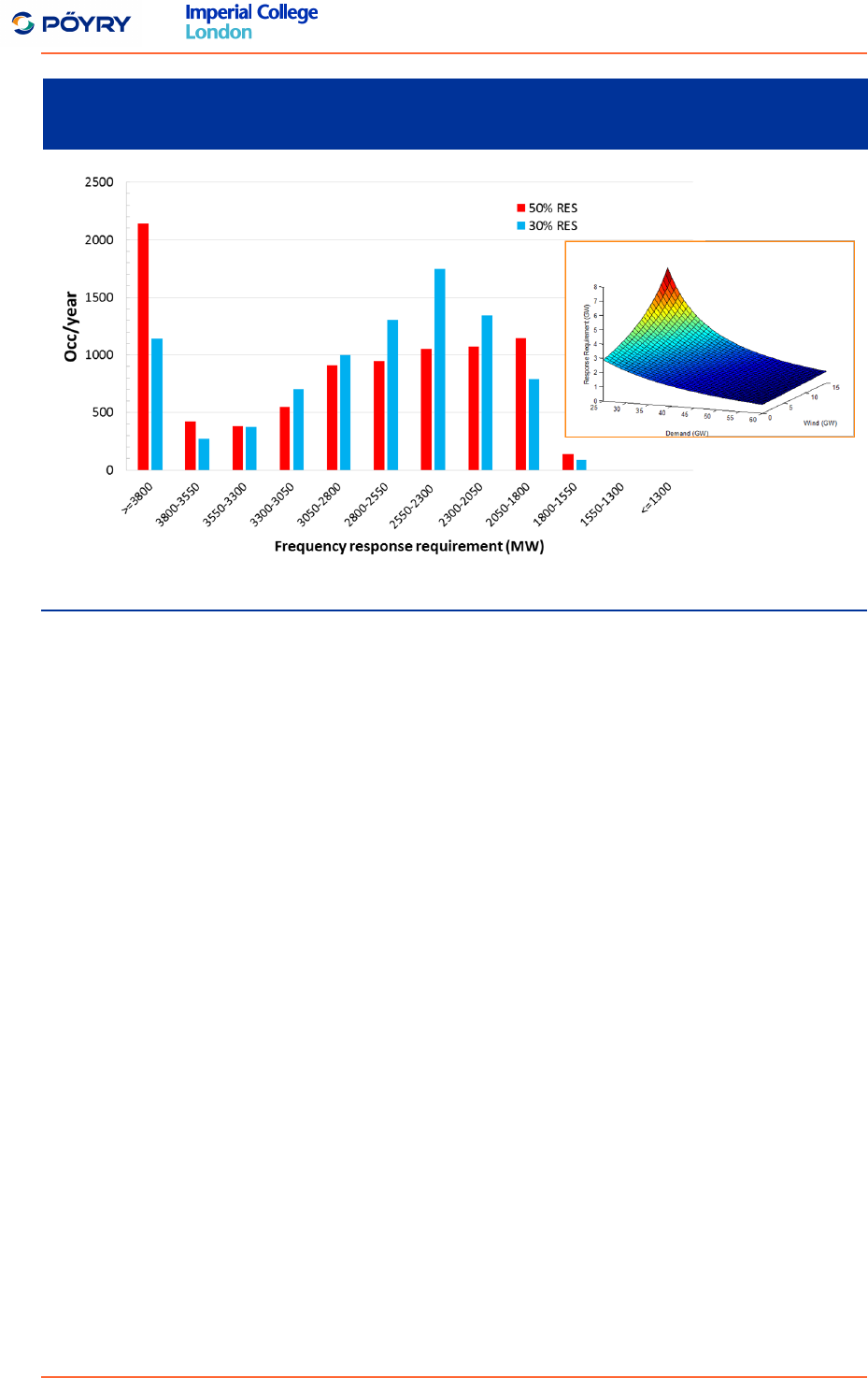

2.2.1.3 Frequency response requirements

Frequency response (FR) refers to the automatic provision of increased generation or

demand reduction in order to contain a drop in system frequency. Increased share of

renewables (i.e. inverter based power generation) in the capacity mix reduces the system

inertia which is provided by the stored kinetic energy of the rotating mass of the power

generator’s turbines. With this reduction in system inertia, any imbalance between supply

and demand will change system frequency more rapidly making the system unstable.

Therefore, a sufficient level of frequency response is needed to deal with sudden loss of

supply to the system (e.g. as a result of a failure of a large generator / interconnector or

rapid demand turn up) in order to keep the system frequency within its statutory limits.

Figure 9 (right box) shows the FR requirement as a function of net demand (demand

minus wind output). It demonstrates that the FR requirement increases significantly when

the net demand is low – e.g. when a low demand condition coincides with high output

from intermittent renewables. On the other hand, the system will require less FR during

high demand conditions coinciding with low output from intermittent generators

considering there are many synchronised plants in the system. As the frequency of

having low net demand is higher in future, it is expected that the requirement for

frequency services by 2030 will also be higher as shown in the Figure 9 (left chart) for

50% renewables penetration.

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

20

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

Figure 9 – Impact of intermittent generation on frequency response requirements

in the future system (illustrative)

Source: Imperial’s modelling analysis

To date, the frequency response service can only be provided by synchronised

conventional plants which need to operate part-loaded and produce at least at the

minimum stable generation level (MSG). This reduces the ability of the system to absorb

electricity production from renewables or other low-carbon technologies. Moreover,

running at a suboptimal level of production (i.e. at MSG level) also reduces the fuel

efficiency of the conventional generation and increases the emissions. This opens

opportunities to alternative FR providing sources such as fast storage or DSR that can

provide the required services potentially at lower cost and without increasing emissions.

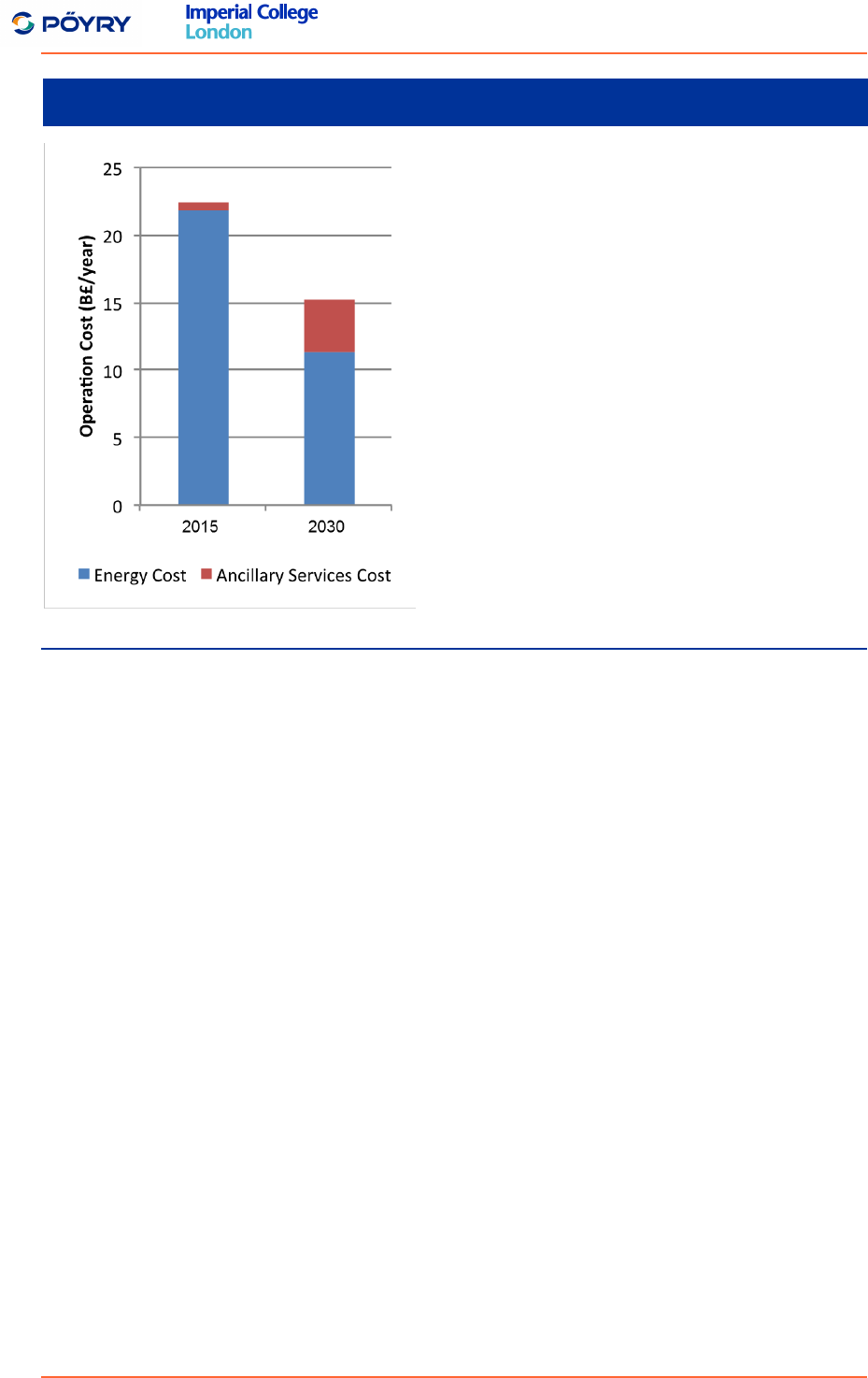

2.2.1.4 Potential increase in the value of flexibility services

The large increase in flexibility requirements will result in a significant growth of the overall

value of such services in the future GB system.

Figure 10 shows the potential change in system operation costs in order to efficiently meet

the CO

2

reduction target of 100gCO

2

/kWh in the power sector in 2030 relative to the 2015

system. Although the overall system operation costs are expected to reduce due to high

penetration of low marginal cost low-carbon generation (wind, solar and nuclear), the cost

of ancillary services costs will potentially increase by about 10 times relative to the 2015

levels.

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

21

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

Figure 10 – Change in overall value of ancillary services (illustrative)

Source: Imperial’s modelling analysis

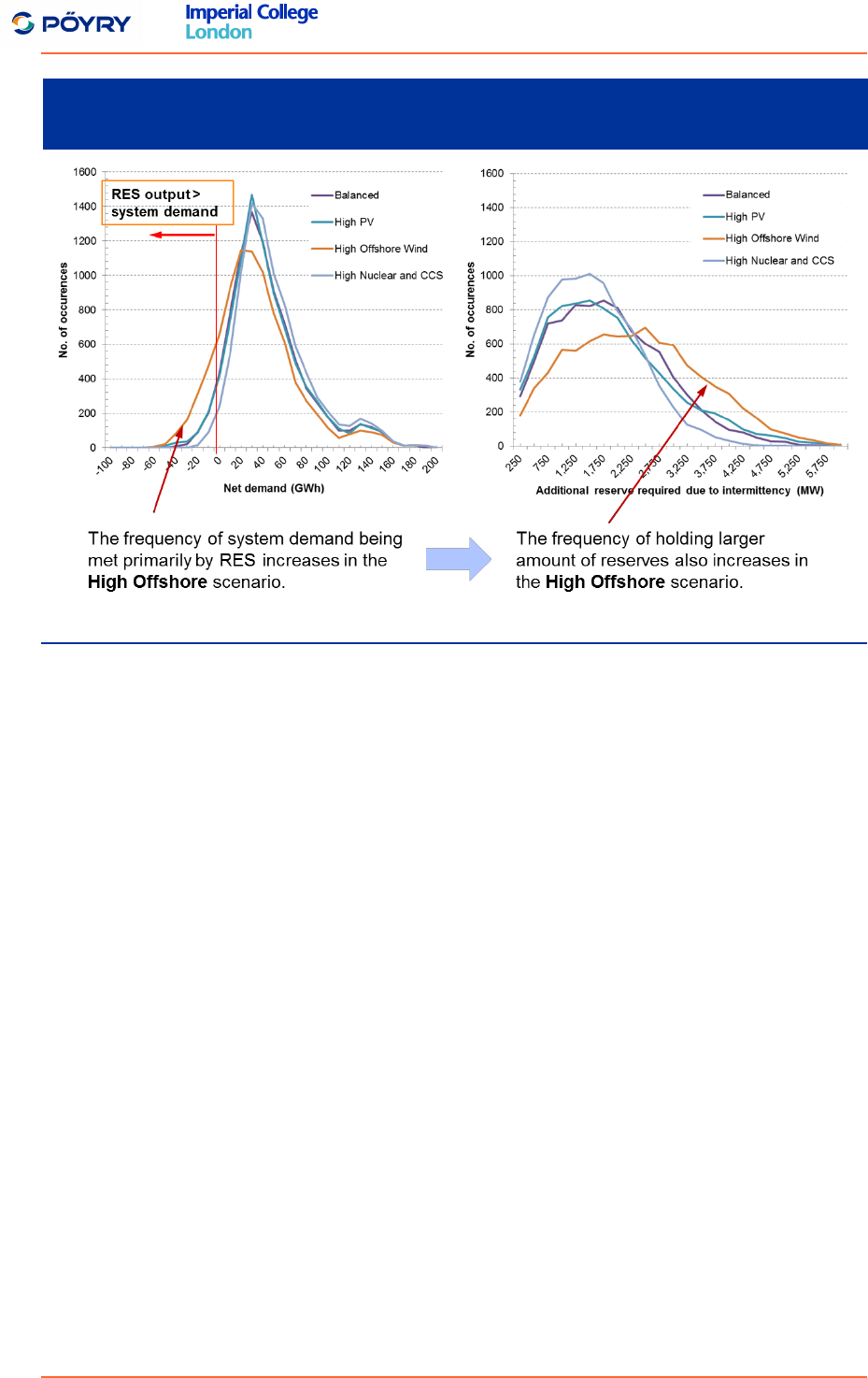

2.3 Impact of alternative generation mixes on flexibility

requirements

The system flexibility requirements depend on many factors such as the characteristics of

the generation system (capacity mix, locations, dynamic parameters, availability, output

profiles of energy sources), demand characteristics (customer types, locations, profiles,

peak demand) and network characteristics (e.g. AC vs. DC links to other systems).

Figure 11 (left chart) compares the frequency distribution of the net demand profiles of the

four modelled scenarios. It can be observed that under the High Wind scenario there are

more periods where the net demand is low or even negative (i.e. total wind output

exceeds system demand).

Figure 11 (right chart) compares the frequency distribution of the operating reserve

requirements across the scenarios, while all low-carbon options result in a rising

(additional) demand for operating reserve, this is most strongly required in the case of

High Wind scenario.

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

22

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

Figure 11 – Evolution of net demand and operating reserve requirements in the

modelled scenarios by 2030

Source: Imperial modelling analysis of the CCC scenarios

2.4 Potential benefits of alternative system flexibility options

Across the modelled scenarios, there are several alternative options for delivering the

necessary flexibility in a decarbonised energy system. To a greater or lesser extent, by

exploiting new sources of flexibility, there is the potential to realise cost savings relative to

a system that continues to rely on conventional generation to deliver flexibility. These

savings are associated with:

Avoidance of energy curtailment from low-carbon generation sources: a lack of

operational flexibility limits the system’s ability to accommodate output from

intermittent renewable technologies, particularly during periods when low demand

conditions coincide with high output from wind and solar sources. Presence of

system flexibility sources such as energy storage facilities, demand side response or

interconnectors can absorb/export surplus generation in the system thus avoiding

energy curtailment and associated costs.

Efficient provision of operating reserve and response facilities: the provision of

operating reserve to the system by non-thermal flexibility technologies (i.e. Storage,

DSR and interconnection) increases the ability of the system to absorb low-carbon

electricity and reduces the need to maintain thermal plant at minimum stable

generation with associated impacts on carbon emissions and operating costs due to

efficiency losses.

Potential savings in generation capacity: new service providers may reduce

overall generation capacity on the system due to:

Reduced need for low-carbon capacity in the system: reductions in energy

curtailment will result in increased utilisation hence lower capacity of low-carbon

generation to meet the decarbonisation targets.

Peak reduction: electrification of heat and transport will disproportionally

increase peak electricity demand however, system flexibility in the form of energy

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

23

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

storage or demand side response can reduce system peak by redistributing

demand from high demand to low demand periods. This results in reducing the

amount of required generation capacity in the system (particularly, the peaking

plant capacity).

Reduced need for back-up capacity: energy storage, DSR and interconnection,

can reduce the need for back-up generation capacity required to support the

intermittent generation.

Deferral or avoidance of the network reinforcement/addition: in addition to the

network capacity savings driven by lower generation capacity requirements (as

described above), additional network capacity savings are possible by deploying

flexibility to manage network constraints and reassessing the need for network

reinforcement in conjunction with innovative network planning and operation

standards as discussed in Section 4.1.2.

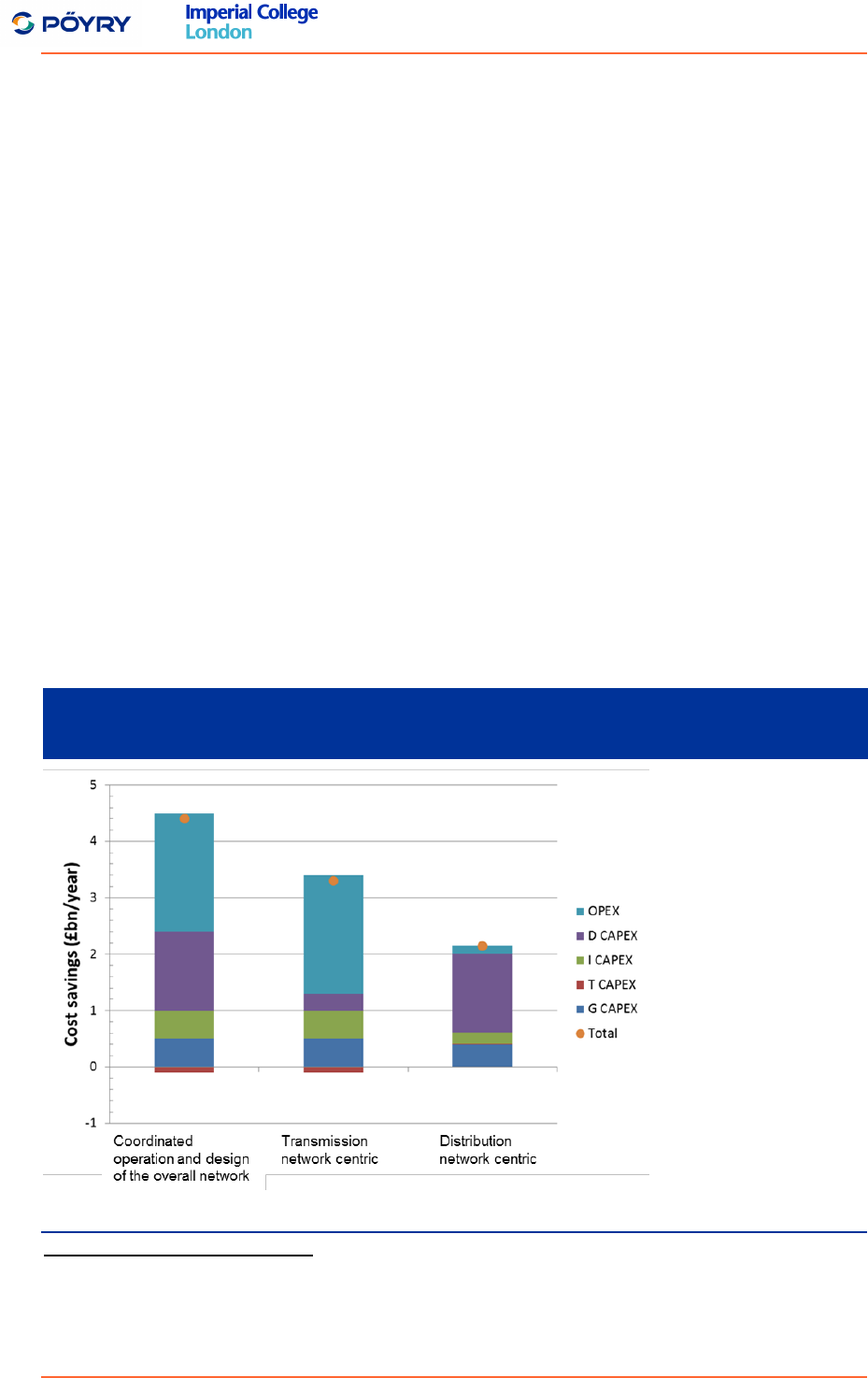

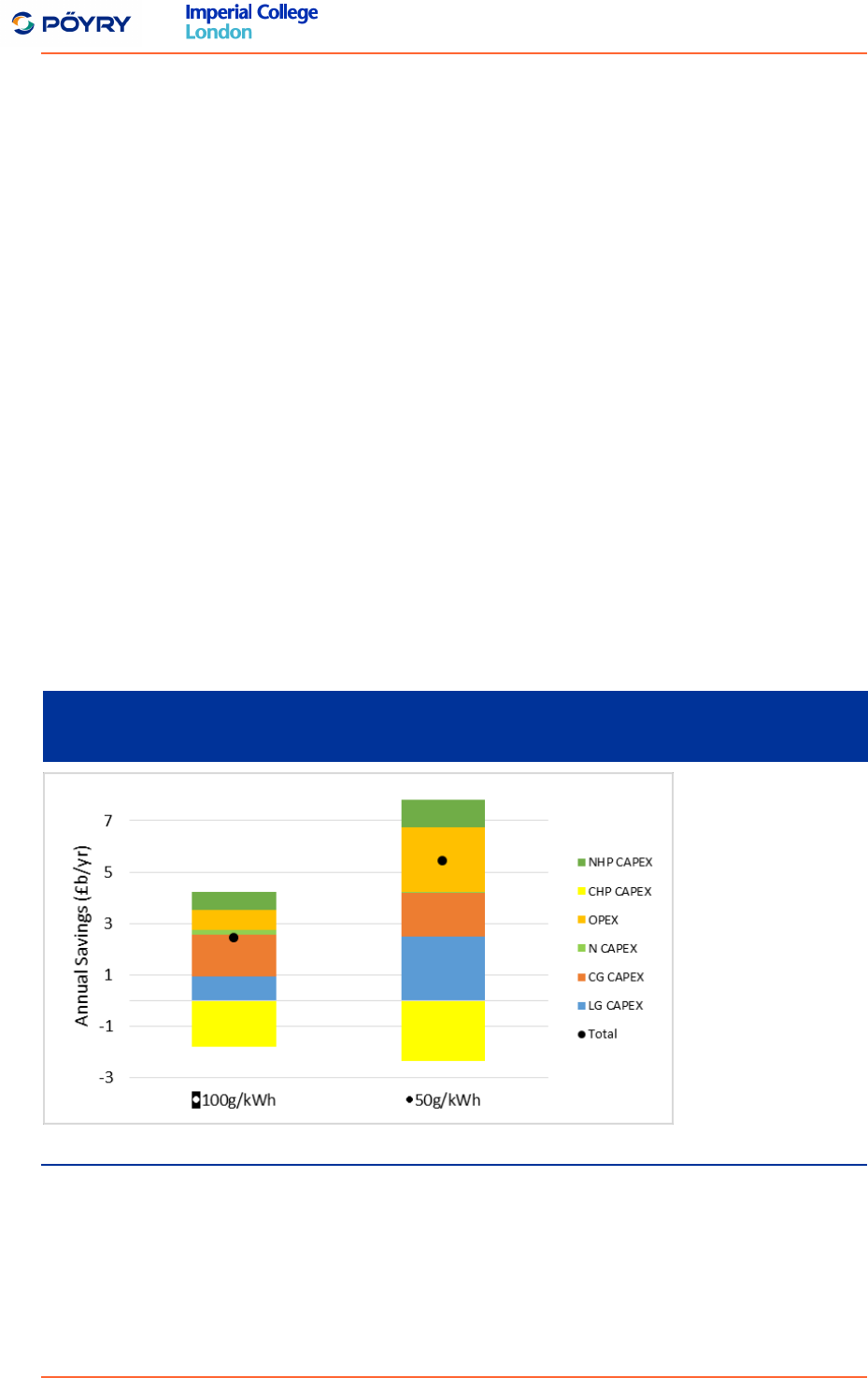

The results of Imperial’s modelling analysis demonstrate that alternative system flexibility

solutions for meeting the CCC’s 2030 carbon intensity target (100gCO

2

/kWh) can save up

to £4.7 bn/year. The savings are obtained from the reduction in system capacity

requirement (low-carbon generation, conventional generation, transmission,

interconnection, distribution assets) and lower operating cost (due to energy curtailment

avoidance, CO

2

cost savings, and reduced fuel usage) as shown in Figure 12 for different

scenarios.

The results also show that the savings due to increased system flexibility are higher in

scenarios with large penetration of intermittent generation (High Wind or High PV

scenarios). This is because the volume of additional system flexibility becomes more

pronounced in such systems compared to a system that also contains non-intermittent

low-carbon, nuclear and CCS, generation (e.g. the Balanced scenario). Presence of

higher flexibility services, from energy storage and/or DSR, enables more efficient

management of demand-supply balance by time shifting the surplus intermittent

generation or demand. This avoids curtailment of solar and/or wind energy as well as

reducing the need for their generation capacity resulting in higher savings in operational

expenditure (Opex) and capital expenditure (capex) respectively.

Moreover, more ambitious carbon reduction target (50gCO

2

/kWh) would see a further

increase the value of flexibility (up to £7.8 bn/year) as the system would need to

accommodate more low-carbon generation.

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

24

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

Figure 12 – System cost savings due to alternative flexibility provision across

scenarios

Source: Imperial’s modelling analysis of the CCC scenarios

2.5 Uncertainties related to the portfolio of flexibility services

As mentioned earlier the required level of additional flexibility is dependent on the

characteristics of the generation capacity mix in the system as multiple generation mixes

can deliver the decarbonisation targets. For a given level of additional flexibility there are

multiple other factors that will define the uptake of different flexibility resource in the future

system, such as:

relative costs, scalability, locational distribution, availability of the control infrastructure

and technical performance of different types of flexibility sources;

the adopted energy policies, market and regulatory framework; and

the social (e.g. consumer acceptance) and cultural (e.g. maintaining status quo)

aspects associated with effective participation of demand side flexibility.

There are uncertainties associated with the aforementioned factors introducing the

uncertainty around the cost of demand side response and/or expected drop in cost of

storage. Similarly, there is lack of clarity as well as diverging views on the level of

consumer acceptance of DSR technologies.

Taking account of the technology cost and deployment rate uncertainties, Imperial College

has analysed the range of possible penetration of different flexibility technologies in their

modelling assessment. Figure 13 shows the modelling based potentials of different

flexibility technologies such as DSR, storage, interconnection and flexible generation in

2030 across different scenarios to meet the 100gCO

2

/kWh carbon intensity target.

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

25

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

Figure 13 – Indication of uncertainty in the deployment of different types of

additional flexibility resource based on scenario modelling

Source: Imperial’s modelling analysis of the CCC scenarios

Given the level of uncertainty over individual flexibility technologies that can be deployed

to the system in future, it is important for the policy, market and regulatory framework

should provide a technology neutral environment to facilitate the development and

deployment of all flexibility technologies.

Earlier analysis by Imperial College

5

also supports the above argument that a ‘balanced’

strategy of deployment across different sources of flexibility is the ‘least worst-regret’

pathway for the UK energy system. Facilitating the ‘balanced’ deployment pathway, with

some deployment of DSR, storage and flexible CCGT by 2020, and deployment of the

current interconnector pipeline

6

, is an effective way to avoid worst regret outcomes and

technological lock-in.

2.6 Main requirements of the future electricity systems

Enabling the transformation to an efficient GB electricity system will not be without its own

challenges. From the analysis and stakeholder engagement undertaken as part of this

study, we have identified four key requirements of any future electricity system.

5

An analysis of electricity system flexibility for Great Britain, D. Sanders, A. Hart, M.

Ravishankar, G. Strbac, M. Aunedi, D. Pudjianto, and J. Brunert, Report by Carbon Trust

and Imperial College London, November 2016, available at:

https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/568982/

An_analysis_of_electricity_flexibility_for_Great_Britain.pdf

6

Electricity interconnectors. Ofgem, available at:

https://www.ofgem.gov.uk/electricity/transmission-networks/electricityinterconnectors

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

26

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

Investment decisions should be made on the basis of the full system value offered by

providers – this means that the market design must effectively price and reward

energy, capacity and flexibility.

Appropriate systems and interfaces should be in place to manage greater complexity

in the system – this implies a capability of the system to deal with more interactions

between distribution and transmission networks and to promote and utilise more

active demand management.

Enhanced framework to achieve greater consumer participation – in addition to

establishing the technical infrastructure for demand-side response, legal and

regulatory frameworks around data protection and consumer protection will be

necessary to achieve widespread consumer acceptance.

Ongoing support for innovation in technology, services and operating models – it will

be important that, as the institutional and market framework evolves, the drive for

innovation across the value chain is not dampened.

In the following chapters, we outline in more detail the importance of each requirement,

the current challenges to realising the objective and the specific actions that will help to

realise the objective. A high-level overview of the ongoing activities relevant to the

proposed actions, where information is available in the public domain, is also described.

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

27

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

3. ENSURING EFFICIENT FLEXIBILITY INVESTMENT

DECISIONS

The shift to a low-carbon electricity system will require major investment, so it is important

that the system makes adequate and timely investment in the most effective technologies

and services. Investment decisions should be made taking account of the value to the

system of the full range of services that the provider is offering. Since more flexibility will

be required, the value of the flexibility offered by technologies should be a key

consideration in any new investments, as should the costs they impose on system

operation. If the value of flexibility is not transparently signalled in the market and

available to all technologies, then the cost to consumers will be higher than it needs to be.

In theory, there are multiple potential revenue streams available to the market players

(both demand and supply sources). These revenues reflect different ‘products’ or

‘services’ and are accessed from a variety of separate market platforms. The main forms

of revenue relate to:

capacity – i.e. provision of system security during system stress conditions through

offers on the capacity market;

wholesale energy provision – i.e. sale of electricity through standard wholesale

markets;

balancing – i.e. actions in the system balancing market;

ancillary services – i.e. provision of specific services to the system operator such as

frequency regulation services; and

network support – i.e. provision of services to reduce the need for network

reinforcement.

These services are not mutually exclusive and for commercial investment decisions to

deliver efficient system development it is important that:

all potential revenue streams exist and are available to a service or technology; and

the value of the service to the system is accurately reflected in the market or

procurement platforms in operation.

This is particularly important for the emerging technologies and services around flexibility

provision as, in contrast to conventional generation investment, a higher proportion of their

value will be dependent on ancillary service and network support revenue streams.

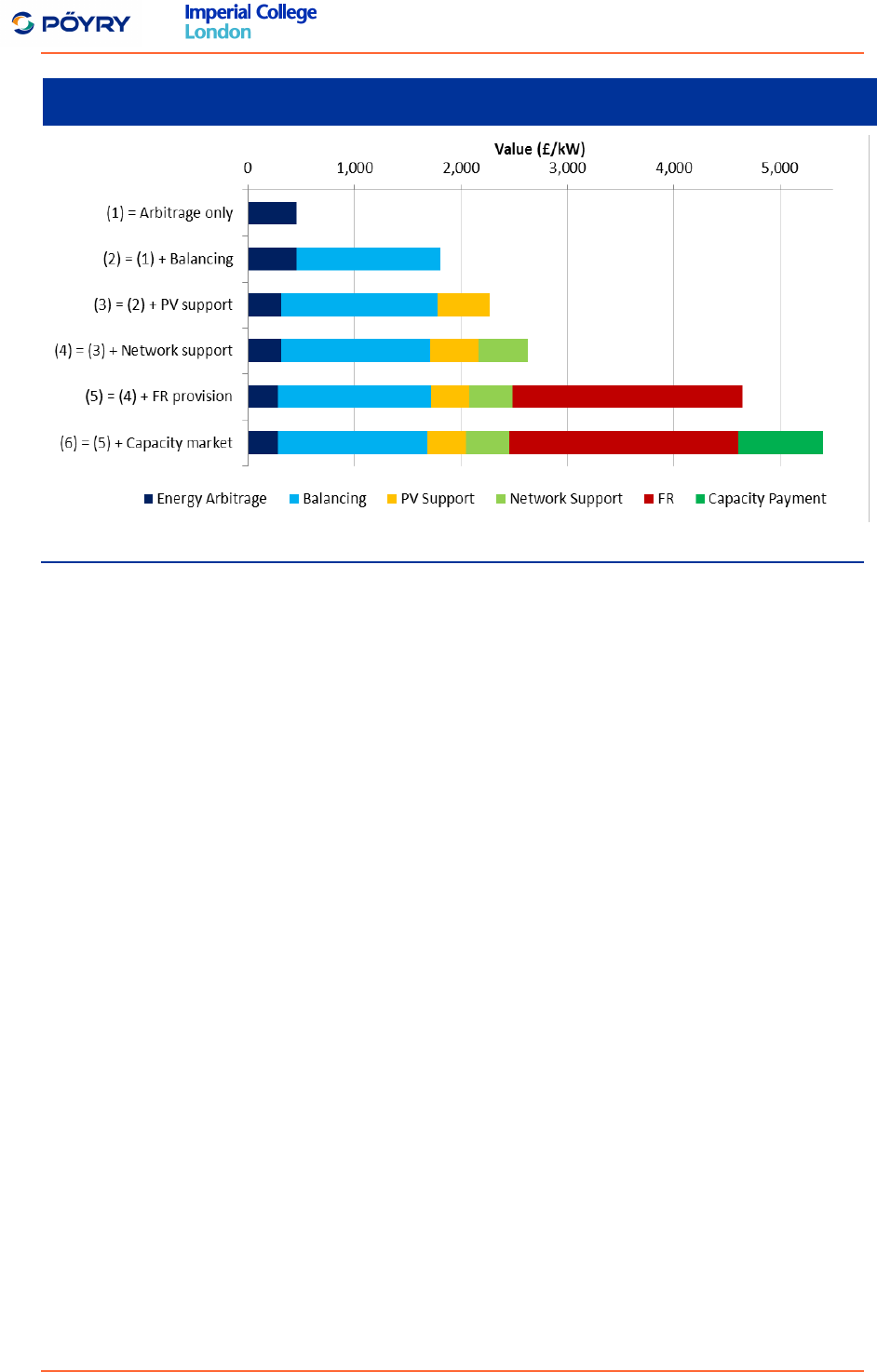

For example, Imperial College has modelled the business case of battery storage facilities

which can provide a range of system services across multiple revenue streams while

taking account of the physical interactions between the different system support services.

Figure 14 shows the results for a 6MW battery storage connected in the HV distribution

grid supporting connection of 20MW of PV generation. This demonstrates how the value

of the asset increases several-fold with access to a wider set of revenue streams.

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

28

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

Figure 14 – A business case for energy storage facilities (illustrative case)

Source: Imperial’s modelling analysis of benefits of full market access

From the analysis and stakeholder engagement undertaken as part of this study, it is clear

that the GB electricity system needs to ensure that:

value streams are available for all forms of system service and that they are

accessible to all potential providers;

the price signals for these services are efficient and reflect the value to the system at

the time; and

there is some transparency for providers over the longer-term requirements for these

services in the market.

The following sections expand on these observations and identify appropriate actions to

address current challenges.

3.1 Availability and accessibility of revenue streams

3.1.1 Availability of flexibility services

In order to ensure future investments in the power system take account of the flexibility

requirements of the system, all types of flexibility services need to be valued. Under the

current arrangements, this is not always the case, with the main gap identified in the

valuing of system inertia.

One of the key challenges associated with integration of renewable generation is the

reduction of system inertia. This may be provided through conventional generators

manufactured with a higher inertia constant or from wind generators providing “synthetic

inertia” (SI). However, the current flexibility market does not reward the provision of

inertia and this has contributed to a lack of interest by investors to develop alternative

ways for enhanced inertia provision. Without a remuneration mechanism for inertia, there

will be higher cost to the system.

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

29

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

3.1.2 Access to revenue streams

Even where revenue streams exist, flexibility providers do not always have access to all of

the services that they can technically offer. This means they may not be able to be

rewarded for the full value they offer to the system, leading either to insufficient flexibility

being available to the system or, more likely, to a higher cost of delivering flexibility due to

inefficient investment and operational decisions.

Examples of limitations to some flexibility providers include:

Independent aggregators need to be a Balancing Mechanism Unit (BMU) or need to

reply on third parties to have access to the balancing mechanism (BM) as they do not

have a defined role in the Balancing and Settlement Code (BSC). This involves

administrative costs and sharing of some revenues with third parties which

discourages small scale aggregators from accessing value in the BM as well as in the

wholesale market.

Enhanced Frequency Response (EFR) providers, which includes all storage facilities,

are excluded from participation in the Capacity Market (CM).

Holders of long-term STOR contracts are ineligible for participation in the Capacity

Market.

Low-carbon capacity sources that receive support payments such as the Renewables

Obligation (RO), Contracts for Difference (CfD) or Feed-in-tariffs (FITs) have no

incentive to provide flexibility even if they are capable of providing.

Ofgem has recently taken several initiatives to assess and improve the flexibility

procurement process in order to provide a more level-playing field for different flexibility

providers. These include identifying barriers and proposing changes in the current

Capacity Market rules for participation of small generators and DSR capacity by initiating

consultations with the relevant stakeholders.

7

,

8

3.1.3 Recommended action on availability and accessibility of revenue streams

Our recommended actions in these areas are outlined below.

Periodical assessment of existing portfolio of flexibility services to identify services that

may be procured more efficiently through transparent and technology-neutral processes

in the future and reform their procurement processes accordingly.

Responsible: SO/DSOs

Initial assessment by 2020

Medium priority

7

Electricity Market Reform: Open letter and consultation on changes to the Capacity Market

Rules, September 2016

https://www.ofgem.gov.uk/system/files/docs/2016/09/open_letter_cm_rules_150916.pdf

8

Capacity Market Rules change proposal submissions, November 2016

https://www.ofgem.gov.uk/electricity/wholesale-market/market-efficiency-review-and-reform/electricity-market-reform/change-proposals

ROADMAP FOR FLEXIBILITY SERVICES TO 2030

May 2017

379_FlexibilityRoadmap_FinalReport_v200.docx

30

PÖYRY MANAGEMENT CONSULTING

IMPERIAL COLLEGE LONDON

3.2 Efficiency of pricing signals

In order to deliver the full benefits of flexibility, price signals should reflect the overall value

of smart technologies to the electricity system. In this section we discuss the enablers for

improving the efficiency of price signals to encourage deployment of flexibility in the future

system.

3.2.1 Provision of dynamic pricing signals

The need and value of flexibility is time dependent – it varies across different seasons as

well as across different times of the day, driven by system demand conditions. With

significant growth in intermittent generation, variation in supply is becoming more

pronounced. At the same, the nature of demand variability is changing as new sources of

demand (e.g. heat pumps and electric vehicles) bring additional variability in demand-

supply balance from the demand side.

In GB, the dynamic value of required flexibility services – e.g. the Firm Frequency

Response (FFR) is procured through a monthly tender based on the demand for this

service which is assessed up to several weeks ahead of real time. This can result in a

risk of over/under procurement of services and a lack of availability of flexibility resource

for other services. Although the balance (i.e. in case of under procurement) can be

procured through mandatory frequency response, it has cost implications. In case of over

procurement, depending on the contract terms, at least the availability fees will be paid to

the providers whose services were not required by the system.

In the future with growing need of flexibility, dynamic price signals (i.e. time dependent

cost of energy and value of flexibility) can potentially incentivise availability of flexibility

during periods when it is most needed by the system. This will also encourage

consumers to change their energy consumption behaviour (i.e. reduce consumption when

the system is under stress or the electricity cost is high and vice versa) in order to lower

overall system costs as well as their bills. In the energy market this is likely to improve as

a result of developments such as half-hourly settlement and reserve scarcity pricing

schedule

9

.

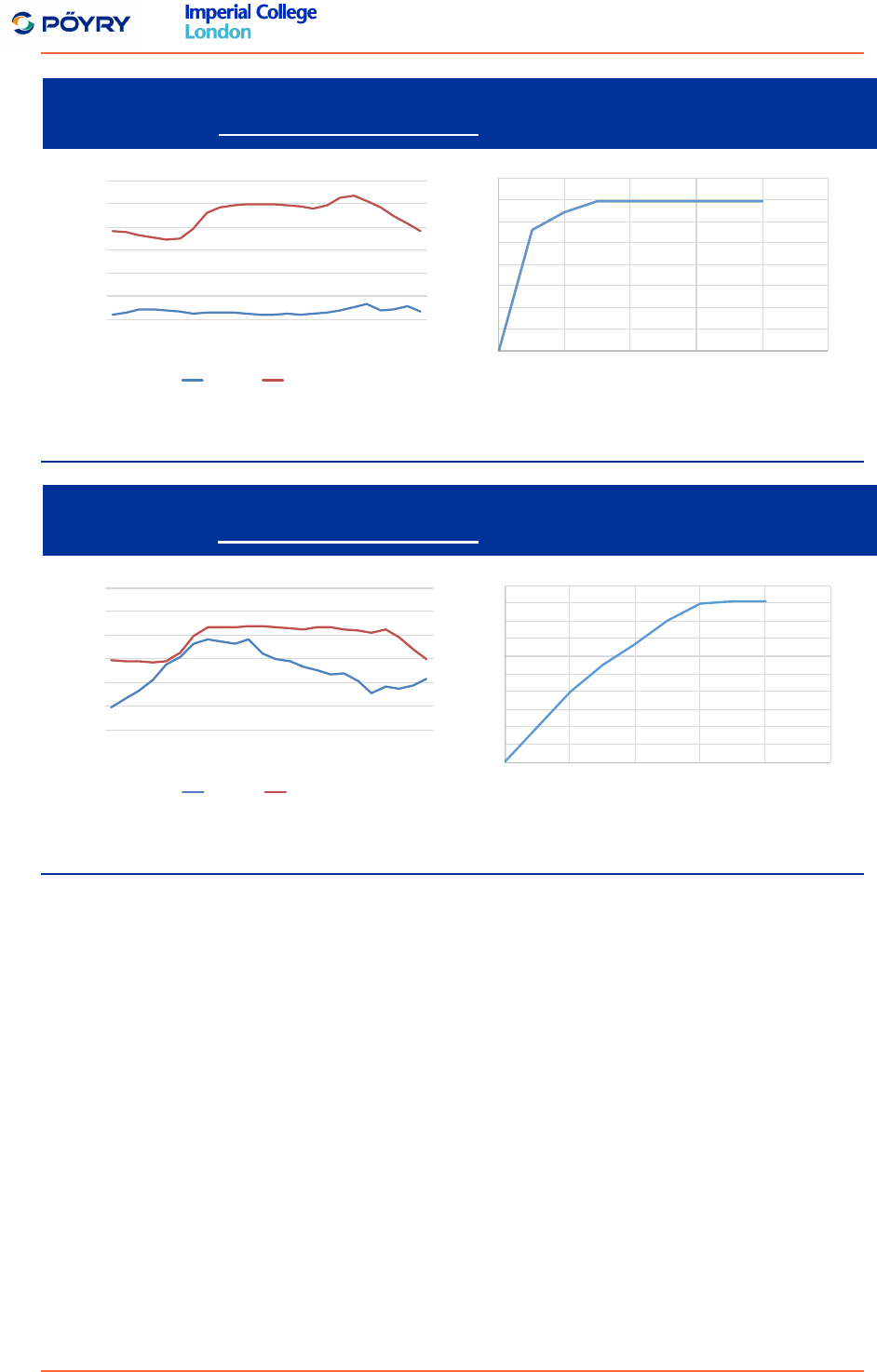

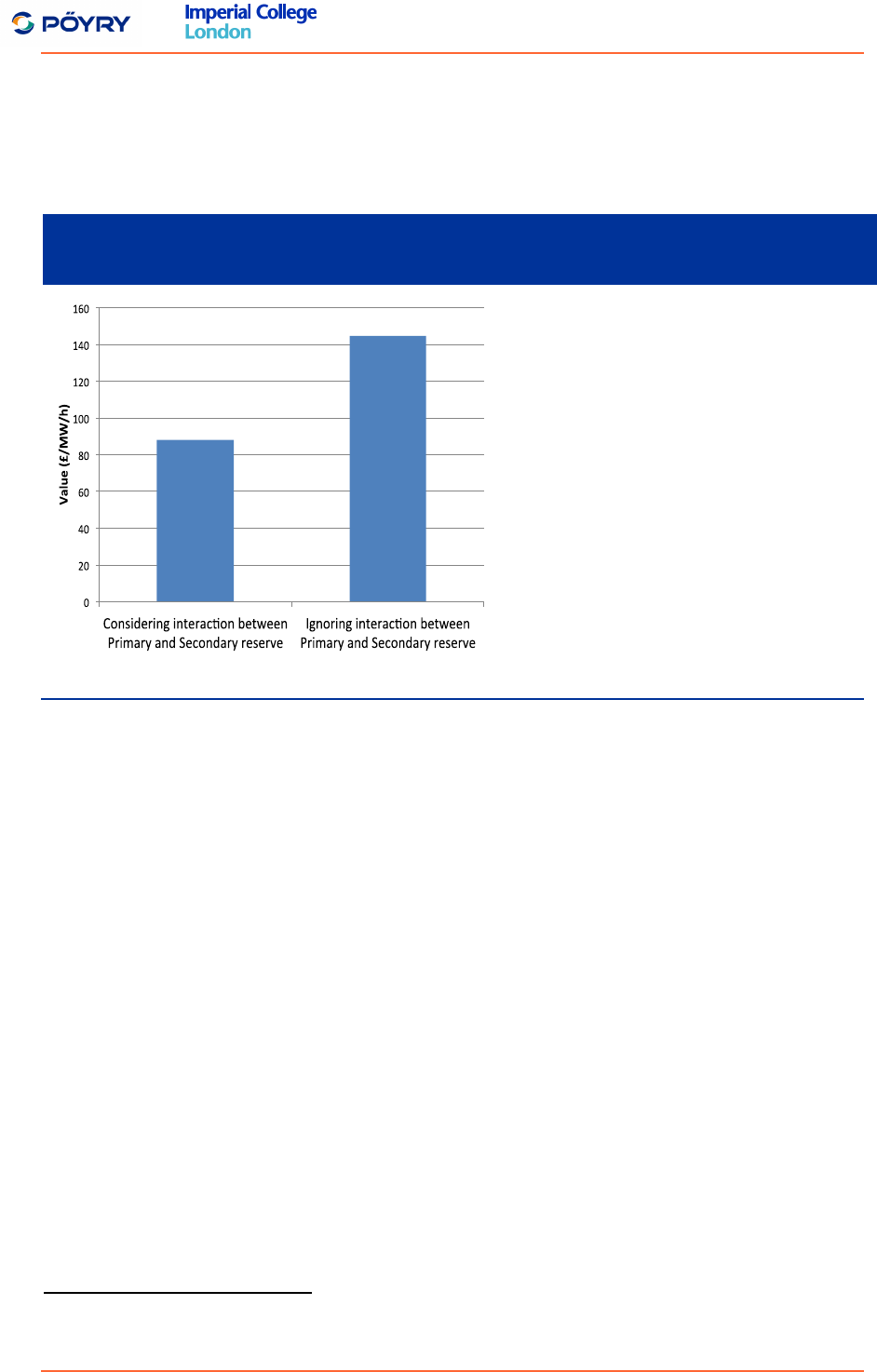

Imperial has investigated the value and need for EFR across days with different system

conditions

10

. As shown in Figure 15 and Figure 16, during high system demand and low

wind days, the benefit of EFR saturates at £350k after 300 MW of EFR become available,

suggesting low demand for EFR. However, during low system demand and high wind

days, more than 600 MW is needed and saves £9000K in operating cost. It is clear that

the value and need for EFR vary significantly across different days and times within a day

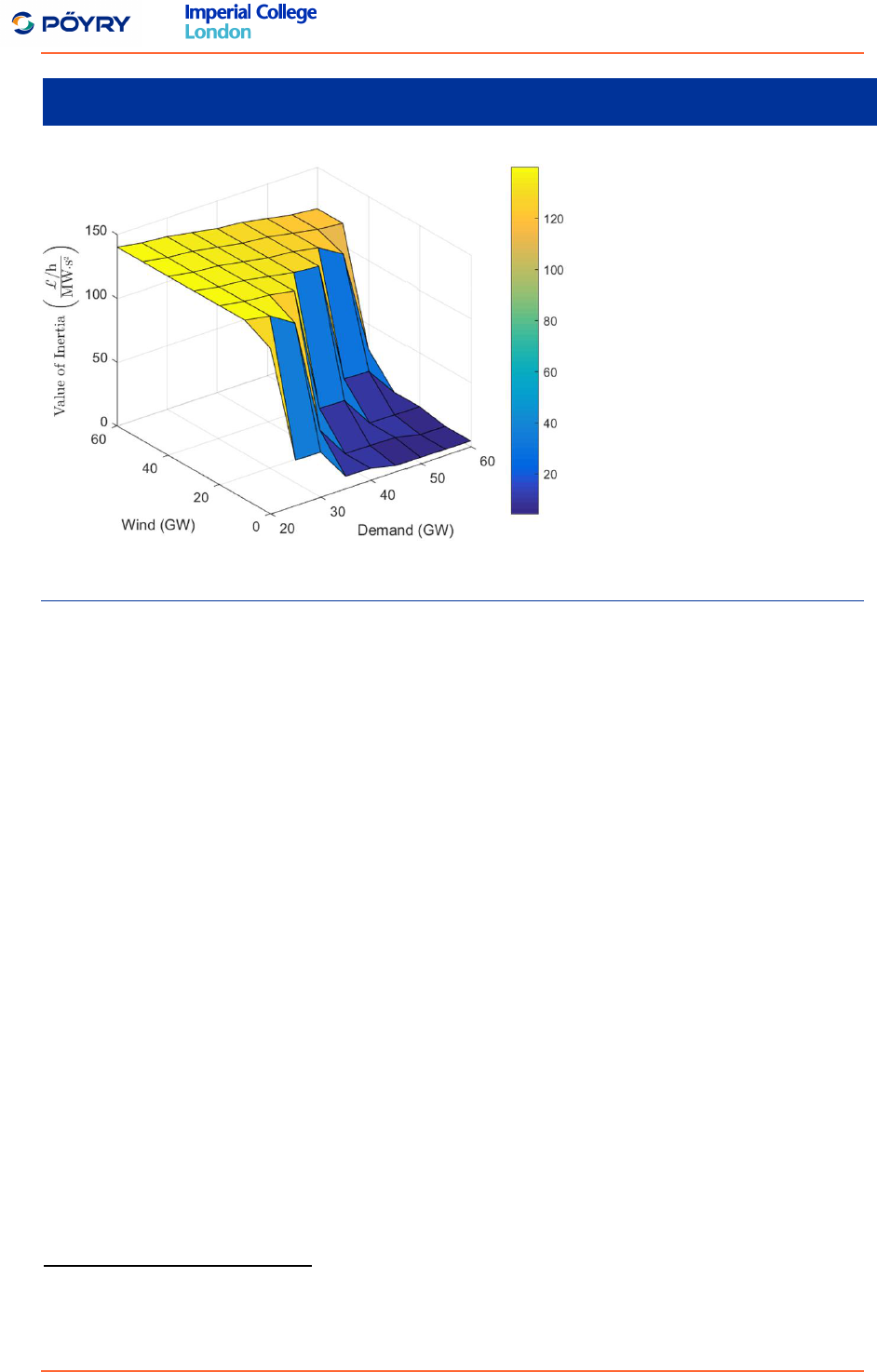

depending on the system conditions. This informs that there is a significant uncertainty in